The dominant read on Iranian oil this week is simple: Tehran’s hand weakens as barrels pile up. More than fifty million barrels float at sea, buyers stay wary, and the August 21 expiration of General License X tightens the clock. Treasury Secretary Scott Bessent’s waiver was supposed to reopen monetization. Instead, cargoes idle while negotiators in Doha pause for funeral processions.

That narrative rests on a fragile foundation. Nearly every quantitative pillar — the fifty-eight-million-barrel hoard, the ninety-percent figure for cargoes without clear destinations, the nine-year-low run rates at Chinese independent refiners — flows from single proprietary datasets (Vortexa, Kpler, JLC) laundered through dozens of outlets into apparent consensus. Treat those numbers as one-source estimates with a wide error band, not established fact. The fleet carrying Iranian crude was built to evade sanctions. Many vessels spoof AIS, transfer cargo ship-to-ship in the Malacca Strait, and signal “for orders” when the true buyer is already known. Inferring a negotiating weakness from tracking data on a fleet designed to lie is epistemologically backwards.

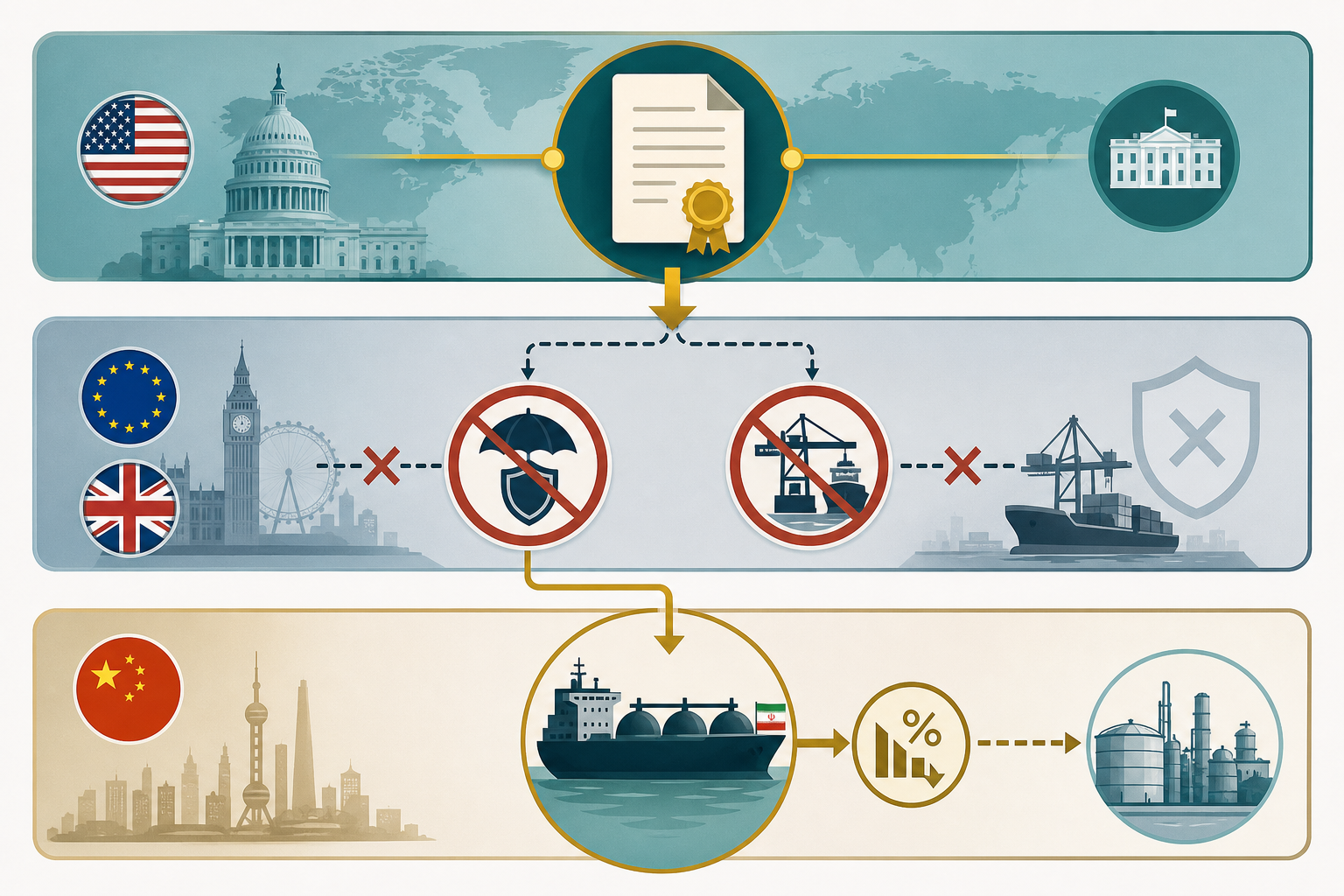

What GL X Actually Unlocked — and What It Cannot

On June 22, OFAC issued General License X, authorizing production, sale, delivery, and offloading of Iranian-origin crude through August 21. The license explicitly covers maritime services — vessel management, crewing, bunkering, insurance, classification, salvage — and permits dollar-denominated payments to Tehran. It is the first concrete sanctions relief under the Islamabad memorandum.

What GL X does not do is waive anyone else’s law. Bird & Bird, Mayer Brown, Clyde & Co, and the UK P&I Club have all issued the same warning: the EU sanctions framework continues to prohibit the purchase, import, transport, and insurance of Iranian-origin oil. Asset freezes on NIOC, NITC, and related entities remain. UK operators face designation-based restrictions that vary by party but still block most conventional trade finance. A transaction lawful under U.S. law can be illegal under EU law — and uninsurable under London market rules that the International Group pool will not cover.

That is the binding constraint Washington cannot negotiate away in a bilateral room. India and Japan have expressed interest in Iranian barrels but await payment clarity and insurance availability. European reinsurers and P&I clubs that cover the majority of global tanker tonnage cannot simply follow OFAC’s lead. GL X is a U.S. safe harbor, not a global one. For every buyer except China — which has long ignored U.S. secondary sanctions on Iranian imports — the license is practically unusable without parallel EU and UK relief that has not been granted.

China’s Slowdown, Not Bessent’s Threats

Iran’s historical fallback is well mapped: discounted barrels to Shandong’s independent “teapot” refiners through shadow channels at three-to-four-dollar discounts to benchmark. That route bypasses Western insurance entirely. It does not bypass Chinese demand.

Shandong teapot run rates fell to roughly fifty percent in late June — the weakest since 2017, per JLC — as refiners lose money on every barrel processed. Beijing capped domestic fuel prices while crude import costs spiked during the Hormuz closure. Electrification has eroded gasoline and diesel demand. China’s state-owned refiners secured supplies through August and are sidestepping Iranian cargoes. Imports of Iranian crude reportedly halved in June to roughly 650,000 barrels per day, per Kpler — a figure that should carry the same single-source caveat as the floating-storage count.

The suppression of Iran’s shadow export channel is therefore less about Treasury threats than about China’s economic deceleration — a factor neither Washington nor Tehran can negotiate away at Doha. Teapots that cannot run profitably will not absorb fifty million barrels at any discount. Bessent’s August 21 deadline matters less than Shandong’s margin sheet.

The Carrot Washington Does Not Control

The structural story is a mismatch of authorities. The United States issued a sixty-day license expecting buyers to return to conventional dollar settlement and Lloyd’s-backed insurance. The European Union did not move. The United Kingdom did not move. The tracking industry counted barrels that may already be sold, may be in transit under false signals, or may not exist at the volumes reported. Markets priced Tehran’s weakness. The verifiable constraint — third-country maritime-services sanctions — went essentially unreported.

Final Compression

Iran’s monetization problem is not primarily that buyers are reluctant. It is that Washington’s license does not unlock the insurance, reinsurance, and port infrastructure that make Iranian oil tradeable for anyone except China’s shadow buyers — and those buyers are running at nine-year lows because of domestic economics, not sanctions diplomacy. The pile-up narrative is an AIS inference on a lying fleet. The maritime blind spot is jurisdictional — and it is the one constraint both sides are pretending not to see.

Tags

Related Articles

Sources

OFAC General License X text and Mayer Brown, Bird & Bird, Clyde & Co, UK P&I on EU/UK sanctions remaining in force; Atlantic Council and Bracewell on GL X scope; Bloomberg, Reuters, Economic Times on floating storage estimates via Vortexa and Kpler; JLC and Reuters on Shandong teapot run rates