The architecture of international order runs on treaties, trade corridors, and trust between intelligence services. In February 2026, all three are under simultaneous stress — and the compounding effects are rewriting how nations cooperate, how they compete, and where capital flows when the old guardrails disappear.

Two Blocs, One Planet, No Consensus

The Western alliance system still commands the most lethal military force on earth. NATO’s 32 members are spending at levels not seen since the Cold War, with a new target of 3.5% of GDP in defense spending by the mid-2030s. The Five Eyes intelligence network — linking the NSA, GCHQ, and their Australian, Canadian, and New Zealand counterparts — remains the deepest signals-intelligence partnership in history, feeding directly into NATO’s joint surveillance architecture. AUKUS has added a nuclear-submarine dimension in the Indo-Pacific.

But the cohesion is fraying from within. Vice President Vance’s 2025 Munich speech signaled declining U.S. commitment to European defense. The Trump administration’s National Security Strategy calls NATO “not an ever-expanding alliance” and tells Europe to take primary responsibility for its own security. This has pushed European capitals into serious debate about a Euro-deterrent — leveraging French and British nuclear arsenals, or even developing nuclear latency across the continent. When your senior ally starts hedging, you start counting warheads.

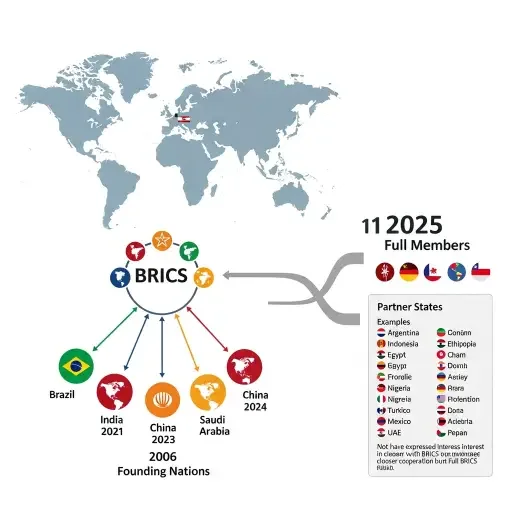

The counterweight is BRICS, and it is no longer a talking shop. The bloc expanded to eleven members with the addition of Egypt, Ethiopia, Iran, Saudi Arabia, the UAE, and Indonesia — with 65 more applications reportedly pending. It now represents roughly 40% of global GDP and nearly half the world’s population. Under India’s 2026 presidency, it hosts both the BRICS Summit and the Quad Summit, threading a diplomatic needle between Western and non-Western blocs. In January, South Africa hosted a BRICS naval exercise off the Cape of Good Hope involving warships from China, Russia, Iran, and the UAE — a clear signal that economic coordination is acquiring a security dimension. India, notably, declined to participate. The coalition is broad, but it is not seamless.

The de-dollarization push is the economic edge of this realignment. Ninety-five percent of India-Russia bilateral trade now settles in local currencies. India’s UPI payment system is being exported across the Global South. A common BRICS currency remains distant — analysts peg it at five to fifty years — but the direction of travel is unmistakable, and every percentage point of trade that exits dollar settlement erodes the structural privilege that underpins American fiscal flexibility.

12,321 Warheads and No Treaty

The nuclear landscape has entered its most dangerous phase since the 1980s. Nine countries hold an estimated 12,321 warheads as of early 2026. On February 5, the New START treaty expired — ending the last bilateral arms-control agreement between the U.S. and Russia, and leaving the two largest arsenals unconstrained by any treaty for the first time in over fifty years.

China’s buildup is the most dramatic variable. Its arsenal has grown from 350 warheads in 2020 to roughly 600 today, adding about 100 per year. Some 350 new ICBM silos have been completed or are near completion. Projections suggest China could match U.S. or Russian ICBM counts by the end of the decade. North Korea has tested a new hypersonic ICBM and announced plans for a nuclear-powered submarine. The Heritage Foundation has proposed expanding the U.S. deployed arsenal to 4,625 warheads by 2050 — triple the current level.

The Bulletin of the Atomic Scientists noted in its 2026 Doomsday Clock statement that the year ended without a single reassuring nuclear development. Three separate theaters saw military operations under the shadow of nuclear weapons. The NPT Review Conference in April will test whether any common ground remains — but arms control, as a practical discipline, increasingly looks like a relic of a bipolar world that no longer exists.

The Iran Flashpoint: Carrier Groups and Countdown Clocks

The most immediate crisis sits in the Persian Gulf. Following the June 2025 “Twelve-Day War” — in which the U.S. and Israel struck Iranian nuclear facilities at Fordow, Natanz, and Isfahan — Iran has been rebuilding under concrete sarcophagi, conducting live-fire drills in the Strait of Hormuz, and holding joint naval exercises with Russia.

Washington has responded with its largest Middle East military buildup since 2003: the USS Abraham Lincoln and USS Gerald R. Ford carrier strike groups, F-35 squadrons at Al Udeid, and a reported 10-to-15-day deadline for a nuclear deal. Two rounds of indirect talks — Muscat on February 6, Geneva on February 17 — produced agreement on “guiding principles” but no breakthrough. The U.S. demands zero enrichment; Iran insists on its nuclear rights. Some analysts identify early March as a potential escalation window. Any military action would immediately threaten the Strait of Hormuz, through which 20% of global oil transits.

Intelligence Networks Face a Structural Redesign

The Five Eyes alliance — the world’s oldest formalized intelligence partnership, dating to 1946 — confronts challenges that cannot be solved by its original Anglophone architecture. Cyberattacks traverse continents in milliseconds, exploiting servers and legal gray zones outside the alliance’s five-nation footprint. A Lawfare analysis argued the alliance “can’t afford to stay small,” and Japan has expressed interest in membership. But expansion introduces divergent classification regimes, data-protection laws, and threat perceptions.

Meanwhile, China and Russia are building parallel intelligence coordination through the Shanghai Cooperation Organization. BRICS naval exercises hint at nascent security-intelligence sharing among non-Western powers. Commercial satellite constellations — from Maxar to Planet Labs — have democratized overhead imagery that was once exclusive to superpowers. Quantum cameras under DARPA development could slash the cost of spy-satellite capability by orders of magnitude. The U.S. Space Force is fielding replacement surveillance constellations, but space is becoming more contested, more commercialized, and entirely ungoverned by updated treaties.

The paradigm is not collapsing, but it is evolving toward something more modular: a Five Eyes core supplemented by variable-geometry coalitions, commercial intelligence partnerships, and AI-enabled analysis platforms.

Trade as Warfare by Other Means

Global trade now operates under tariff conditions not seen since the mid-1940s. The effective U.S. tariff rate reached 13.5% by February 2026 — before the Supreme Court’s February 20 ruling struck down IEEPA tariffs in a 6-3 decision. Alternative legal pathways remain, and Section 232 tariffs on autos, steel, aluminum, and semiconductors persist. The U.S. trade deficit surged to $70.3 billion in December 2025, a 32.6% monthly increase.

Supply chains are not re-shoring — they are re-routing. Deficits with Mexico, Vietnam, and Taiwan have ballooned to records even as the China deficit narrowed, suggesting production has shifted but costs have risen. The USMCA renegotiation scheduled for 2026 carries genuine failure risk: if it collapses, 90% of tariff-free North American trade loses its legal basis. South-South trade continues to grow as a counterbalance, rising from $0.5 trillion in 1995 to $6.8 trillion in 2025.

The World Economic Forum’s 2026 Global Risks Report ranked geoeconomic confrontation as the top risk of the year. Sixty-eight percent of respondents expect a “multipolar or fragmented order” over the next decade. Only one percent anticipated calm.

What This Means for Capital

These forces are not background noise for portfolios — they are becoming the primary allocation signal. Wellington Management captures the structural reality: geopolitical cycles last 80 to 100 years, and the current disruption is a once-per-century event.

The near-term picture through 2027 is defined by elevated volatility across asset classes. The Iran crisis introduces oil-supply tail risk. Tariff uncertainty suppresses corporate investment. Defense stocks and gold — the standout performers of 2025 — are likely to maintain that status. Inflation remains structurally stickier than central banks would prefer, with tariffs alone adding an estimated 0.5 percentage points to core PCE. The Federal Reserve’s room to cut is constrained. Treasury market stress builds as foreign holders — currently above 30% of the market — weigh de-dollarization incentives against the absence of viable alternatives.

The medium-term through 2030 favors defense technology, AI infrastructure, cyber security, critical minerals, and space — the sectors where national-security spending is creating secular demand. Emerging markets will diverge sharply: countries positioning as alternative manufacturing hubs (India, Vietnam, Mexico) will attract re-routed supply chains, while commodity-dependent economies face tariff headwinds and eroding multilateral protections.

The long-term picture is structural. A multipolar world with weakened institutions, expanded nuclear arsenals, and fragmented trade will carry permanently higher risk premiums. Portfolio construction must adapt: greater exposure to real assets, geographic diversification beyond traditional Western markets, and active management to navigate the differentiation between winners and losers that passive strategies will increasingly miss.

Tags

Related Articles

Sources

Federation of American Scientists (nuclear warhead inventories), SIPRI Yearbook 2025, Bulletin of the Atomic Scientists 2026 Doomsday Clock statement, Council on Foreign Relations, Chatham House, World Economic Forum Global Risks Report 2026, IMF World Economic Outlook January 2026, KPMG 2026 Trade Outlook, Tax Foundation tariff analysis February 2026, UN Trade and Development January 2026, Wellington Management geopolitical outlook, EY-Parthenon 2026 Geostrategic Outlook, Lawfare, Al Jazeera, NBC News, NPR, Axios reporting on Iran-US negotiations February 2026, Air & Space Forces Magazine.