On Wednesday evening, Nvidia delivered the kind of quarter most companies fantasize about in pitch decks they’ll never fulfill. Revenue hit $68.13 billion — a 73% surge from the year-ago period and roughly $2 billion above the consensus. Adjusted earnings landed at $1.62 per share, nine cents ahead of expectations. Data center revenue — the division that now constitutes 91% of the company — climbed 75% to $62.3 billion. Full-year revenue crossed $215 billion, nearly doubling what it reported just two fiscal years ago. And guidance for the current quarter came in at $78 billion, a number that would have sounded hallucinatory eighteen months ago.

By Thursday’s close, the stock had shed 5.5%, settling at $184.89, its worst session since mid-April. Trading volume doubled its three-month average. The Nasdaq fell 1.18% in sympathy; AMD and Intel lost more than 3% each. Morgan Stanley’s Joseph Moore said he was “surprised” by the muted response, calling the print “the largest, cleanest beat and raise in the history of the semis industry.”

The paradox is the story.

The Bar That Moves Faster Than the Runner

Nvidia’s problem is not execution. It is the architecture of expectations. At a roughly $4.8 trillion market capitalization, the stock has already absorbed years of forward growth into its price. A 73% revenue surge doesn’t move the needle when the market has already priced in 80% or more. Tom Graff, Facet’s chief investment officer, told CNBC that the market is “very much in ‘prove it’ mode,” and Nvidia “just didn’t quite prove it.”

Adam Phillips of EP Wealth Advisors framed it more bluntly: “The odds were stacked against them. The bar is just so high right now.” Dan Hanbury at Janus Henderson flagged the deeper structural worry — it isn’t Nvidia’s margins that investors are questioning; it’s whether the hyperscalers who write the checks can sustain the spending rate that feeds them.

$700 Billion and the Question Nobody Can Answer

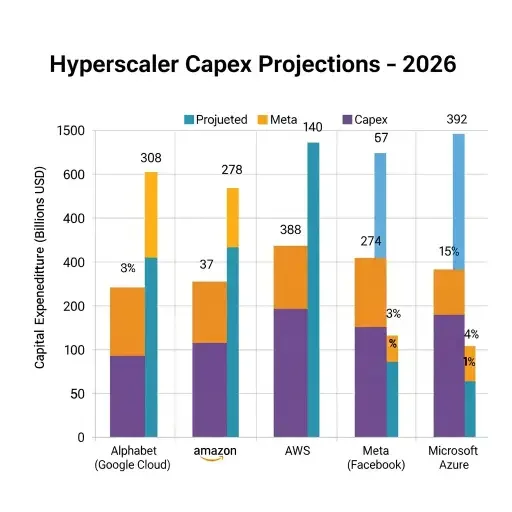

That spending is no longer theoretical. Combined capital expenditures for Alphabet, Amazon, Meta, and Microsoft are converging on $700 billion for this year alone. A recent Moody’s report flagged $662 billion in future data center lease commitments sitting off-balance-sheet. Jensen Huang, on the earnings call, was characteristically unbothered. “Computing demand is growing exponentially,” he said. “Our customers are racing to invest in AI compute — the factories powering the AI industrial revolution.”

But the market is no longer listening to demand narratives in isolation. It wants the other half of the equation: where does the revenue come from on the other side of all that infrastructure? Hyperscaler free cash flow has become the new obsession. If the companies buying Nvidia’s chips can’t translate that compute into monetizable products, the capex engine eventually stalls — and Nvidia’s revenue with it. JPMorgan argued this week that the fear is based on “broken logic,” but fear, once it colonizes a market thesis, doesn’t require logical coherence to move billions.

The SaaSpocalypse Shadow

Compounding the mood is a question Nvidia didn’t create but can’t escape: what if AI compute doesn’t just build the future — it destroys the present? Since early February, the “SaaSpocalypse” triggered by Anthropic’s Claude Cowork platform has wiped $285 billion off software stocks. Thomson Reuters, LegalZoom, Salesforce, Intuit — all cratered as investors concluded that agentic AI tools could bypass the per-seat SaaS licensing model that undergirds much of enterprise software.

Huang himself called the selloff “the most illogical thing in the world,” insisting the software industry won’t be replaced. Anthropic CEO Dario Amodei staged a coordinated stabilization effort on February 24, reframing Claude as “augmentation, not replacement.” Markets partially recovered. But the damage lingers as background radiation in every AI-adjacent valuation conversation. If agentic AI compresses the need for software seats, it might also compress the need for the compute that powers those seats — or at least force investors to rethink the timeline.

Vera Rubin, Margins, and What Actually Went Right

Buried beneath the sentiment wreckage were genuine signals of strength. Gross margins recovered to 75% GAAP, up from 73.4% last quarter, beating guidance. Professional visualization revenue jumped 159% year over year to $1.32 billion. Sovereign AI revenue tripled, hitting $30 billion annually. And Nvidia shipped its first Vera Rubin samples to customers, confirming that its next-generation rack-scale systems remain on track for later this year.

The forward P/E ratio now sits in the low 20s — a valuation that, for a company still growing above 70%, would look like a bargain in any context except one poisoned by existential doubt about the entire AI investment thesis.

The Verdict the Market Is Writing

Nvidia did not fail on Wednesday. It delivered what is, by any conventional measure, a historic quarter. The market’s response was not a judgment of the company’s performance — it was a confession about the market’s own uncertainty. The AI trade has entered a phase where excellence is table stakes, where 73% growth is met with a shrug and a 5.5% haircut, where the question is no longer can they build it but will any of this matter.

The answer is probably yes. But “probably” and “$4.8 trillion” make for an uneasy marriage, and until the hyperscalers start showing revenue growth that matches their spending growth, Jensen Huang will keep winning quarters and losing trading sessions. The most valuable company on earth is now a Rorschach test for the entire AI economy — and today, the market saw the inkblot and flinched.

Tags

Related Articles

Sources

CNBC earnings reports, Bloomberg market analysis, Fortune Q4 coverage, Kiplinger live earnings commentary, Motley Fool market analysis, Yahoo Finance market data, 24/7 Wall St. market coverage. All data sourced from Nvidia's official Q4 FY2026 filing, analyst estimates from LSEG and FactSet, and on-the-record analyst quotes from EP Wealth Advisors, Janus Henderson, Facet, and JPMorgan.