Record Earnings Signal Margin Expansion

TSMC reported fourth-quarter net income of NT$505.74 billion—approximately $16.01 billion—representing a 35 percent year-over-year increase that exceeded analyst estimates by roughly 6 percent. Revenue reached NT$1,046.09 billion, or $33.73 billion, marking the eighth consecutive quarter of profit growth and establishing new quarterly records across revenue, margins, and earnings per share.

The company’s profitability metrics demonstrated the pricing power that comes from technological leadership. Gross margin expanded to 62.3 percent, operating margin reached 54.0 percent, and net profit margin hit 48.3 percent. These margins reflect TSMC’s position as the sole manufacturer capable of producing chips at the most advanced nodes where performance requirements justify premium pricing.

Advanced process technologies—defined as 7-nanometer or smaller—contributed 77 percent of total wafer revenue in the fourth quarter, up from 74 percent for full-year 2025 and 69 percent in 2024. The migration toward leading-edge nodes accelerates as AI workloads demand transistor density and energy efficiency that older manufacturing processes cannot deliver at competitive performance levels.

Within advanced nodes, 3-nanometer chips accounted for 28 percent of fourth-quarter wafer revenue while 5-nanometer represented 35 percent and 7-nanometer contributed 14 percent. The company entered high-volume manufacturing of 2-nanometer technology in the fourth quarter with what management described as good yield at both Hsinchu and Kaohsiung fabrication sites. Strong demand from smartphone and high-performance computing AI applications is expected to drive a fast ramp in 2026.

CFO Wendell Huang guided first-quarter 2026 revenue to a range of $34.6 billion to $35.8 billion, implying approximately 4 percent sequential growth and 38 percent year-over-year growth at the midpoint. For the full year, CEO Wei forecast revenue growth of close to 30 percent in U.S. dollar terms, well above the 14 percent growth rate the company expects for the broader foundry industry.

Capex Surge Targets 2028-2029 Supply

The capital expenditure increase represents the most significant element of the guidance. TSMC spent $40.9 billion in 2025, already a substantial jump from $29.8 billion in 2024. The projected $52 billion to $56 billion for 2026 marks another 27 percent to 37 percent increase. Approximately 70 to 80 percent of the 2026 budget will fund advanced process technologies, with 10 percent allocated to specialty technologies serving automotive, industrial, and IoT applications, and 10 to 20 percent supporting advanced packaging, testing, and mask-making capabilities.

Wei explained the capital intensity stems from escalating manufacturing complexity. The capex required to build 1,000 wafers per month of 2-nanometer capacity substantially exceeds the equivalent investment for 3-nanometer, reflecting higher tool costs, increased process steps, and more stringent contamination control requirements. Depreciation expense is expected to increase by a high-teens percentage year-over-year in 2026 as the company ramps 2-nanometer production.

The timing mismatch between capital deployment and capacity contribution creates strategic vulnerability that TSMC appears willing to accept. Wei told analysts that even with $52 billion to $56 billion in 2026 spending, the contribution to current-year supply will be almost none, with only marginal impact in 2027. The company is building for 2028 and 2029 supply, hoping that timeframe will narrow the gap between demand and available capacity.

This multi-year planning horizon reflects fabrication construction timelines. Building a new fab requires two to three years from groundbreaking to initial production. Equipment installation, cleanroom validation, process qualification, and yield ramp add additional quarters before meaningful volume shipments begin. The capital TSMC commits in 2026 won’t materially affect the supply-demand imbalance that currently characterizes leading-edge capacity.

AI Accelerators Drive 50%+ Growth Trajectory

High-performance computing—which includes AI accelerators, data center CPUs, and graphics processors—accounted for 55 percent of fourth-quarter revenue and 58 percent of full-year 2025 revenue. This represents 4 percent quarter-over-quarter growth and 48 percent year-over-year expansion, demonstrating that AI infrastructure buildout is accelerating rather than plateauing despite concerns about excess capacity and utilization rates.

Wei disclosed that AI accelerator revenue specifically reached a high-teens percentage of total revenue in 2025. The company raised its forecast for AI accelerator revenue growth to a compound annual growth rate approaching the mid-to-high 50s percent through 2029. This projection assumes continued data center expansion by hyperscalers, enterprise adoption of AI workloads, and eventual consumer device integration of on-device AI capabilities.

Counterpoint Research senior analyst Jake Lai characterized 2026 as a breakout year for AI server demand, noting that demand for AI remains very strong and is driving overall chip demand across the entire server industry. This aligns with Goldman Sachs Research estimates showing global data center power usage at approximately 55 gigawatts currently, with AI workloads accounting for 14 percent of that total and growing at roughly 30 percent annually compared to 9 percent for conventional server workloads.

The supply constraint commentary validates infrastructure spending by cloud providers that has drawn investor skepticism. Microsoft, Google, Amazon, and Meta collectively spent more than $200 billion on capital expenditures in 2025, with substantial portions directed toward data center construction and AI accelerator purchases. Critics have questioned whether utilization will justify these investments or whether capacity will sit idle as AI application development lags infrastructure deployment.

TSMC’s capacity planning through 2029 suggests the company sees durable rather than cyclical demand. Chipmakers typically align capital spending with expected revenue two to three years forward, incorporating customer forecasts, technology roadmaps, and market share assumptions. A 40 percent capex increase signals confidence that current AI infrastructure investment represents the early phase of multi-year expansion rather than a near-term bubble approaching exhaustion.

Geographic Expansion Addresses Geopolitical Risk

The geographic distribution of capacity expansion reflects both customer requirements and geopolitical considerations. Wei confirmed TSMC has entered the permitting phase for a fourth fabrication plant in Arizona as part of a broader $165 billion U.S. investment plan. The Arizona footprint will eventually include advanced packaging capacity—critical for AI chips where performance increasingly depends on how processors, memory, and networking components are integrated rather than transistor scaling alone.

In Japan, the first specialty fab in Kumamoto began volume production in late 2024 with very good yield. Construction of a second Kumamoto fab has started, with the ramp schedule dependent on customer needs and market conditions. In Germany, construction of a specialty fab in Dresden is progressing as planned. These international expansions diversify supply chains and address customer demands for geographic redundancy following pandemic-era disruptions and rising U.S.-China technology restrictions.

Wei flagged global tariff policies as a potential risk factor for 2026, noting uncertainties tied to rising component prices particularly in consumer-related and price-sensitive segments. The company indicated it would remain prudent in planning while focusing on fundamentals. This caution reflects exposure to policy volatility as governments increasingly view semiconductor manufacturing as strategic infrastructure subject to industrial policy interventions.

TSMC’s Taiwan operations remain the technological core. The company is preparing multiple phases of 2-nanometer fabs in both Hsinchu and Kaohsiung Science Park. The N2P variant is scheduled for volume production in the second half of 2026, while A16—featuring Super Power Rail technology that improves power delivery efficiency—is on track for volume production in the same timeframe.

Advanced packaging represents a growing portion of value-add as Moore’s Law economics shift. While transistor scaling continues delivering density improvements, the cost per transistor benefit has diminished. Chiplet architectures that combine multiple dies in a single package through advanced interconnect technologies offer performance and cost advantages that monolithic scaling cannot match. TSMC’s investment in advanced packaging capabilities positions the company to capture more of the total system value as packaging becomes more central to chip performance.

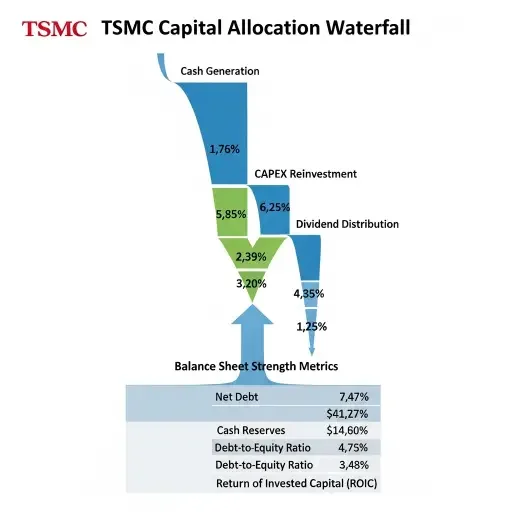

The company generated NT$726 billion in operating cash flow during the quarter and held approximately $98 billion in cash and marketable securities. This financial position supports the elevated capex program without requiring external financing that would introduce covenant restrictions or dilute equity. TSMC raised shareholder dividends to NT$18 per share in 2025 from NT$14 in 2024 and indicated shareholders will receive at least NT$23 per share in 2026, demonstrating that capital deployment for growth doesn’t preclude returning cash to investors.

Huang emphasized that despite shouldering a greater burden of capex investment for customers, TSMC believes long-term gross margins of 56 percent and higher through the cycle are achievable, supporting return on equity in the high 20s percent range. This profitability outlook assumes the company can leverage manufacturing excellence to generate more wafer output and drive greater capacity optimization across nodes while maintaining pricing discipline on leading-edge technologies.

The margin trajectory faces near-term headwinds. Huang noted that overseas fab ramps are expected to dilute gross margin by 2 to 3 percentage points in early stages and 3 to 4 percentage points in later stages, as new facilities operate below optimal efficiency while processes stabilize and yields improve. The initial ramp of 2-nanometer technology will similarly pressure margins before maturity brings costs down to sustainable levels.

N3 gross margin is expected to cross over to the corporate average sometime in 2026 as volume scales and yields mature. This milestone matters because it demonstrates that even the most advanced nodes can reach profitability levels that justify the capital intensity required to build them. If 3-nanometer can achieve corporate average margins within roughly two years of volume production, it validates the economic model for 2-nanometer and subsequent nodes.

TSMC’s relationship with 534 customers across 305 distinct process technologies creates diversification that insulates the company from single-customer or single-application risk. While AI accelerators drive the current growth narrative, automotive, industrial, and consumer applications continue generating steady demand for specialty and mature nodes. This portfolio effect allows TSMC to sustain capital spending through technology transitions and market cycles.

The competitive landscape reinforces TSMC’s pricing power. Samsung Foundry and Intel Foundry Services represent the only other manufacturers pursuing leading-edge logic capacity, but both trail TSMC in process maturity, yield, and customer adoption at the most advanced nodes. China’s Semiconductor Manufacturing International Corporation faces technology restrictions that prevent access to the advanced lithography equipment required for sub-7-nanometer production. This oligopoly structure at the technology frontier enables TSMC to capture most of the value created by transistor scaling.

Energy Infrastructure Emerges as Parallel Constraint

Energy infrastructure represents an emerging constraint on data center expansion independent of chip supply. Data centers consumed approximately 183 terawatts hours of electricity in the United States during 2024—roughly 4.4 percent of national energy use—with projections showing consumption could reach 426 terawatt hours by 2030. AI workloads are particularly power-intensive, with advanced GPUs consuming 350 to 700 watts compared to 150 to 350 watts for traditional CPUs.

This power demand creates regional grid stress that influences data center siting decisions and potentially limits deployment even when chip supply becomes available. Arizona lawmakers are currently debating whether to roll back tax incentives for data centers amid neighborhood opposition and concerns about electricity and water consumption. If key states reduce incentives or impose capacity constraints, hyperscalers may need to reprice projects or shift to more favorable jurisdictions, potentially slowing the pace of AI infrastructure deployment regardless of chip availability.

The intersection of chip supply constraints, energy infrastructure limitations, and capital intensity creates complex dynamics for the AI buildout. TSMC’s capex commitment signals confidence that demand will absorb the capacity being built, but the CEO’s acknowledgment that balance won’t arrive until 2028 or 2029 indicates persistent supply tightness that could constrain application development and model training throughout the intervening period.

Markets Validate Structural Demand Thesis

Markets responded positively to the earnings and guidance. TSMC shares rose more than 6 percent in Thursday trading, with the VanEck Semiconductor ETF climbing 3 percent and Nvidia gaining more than 2 percent on the validation that AI chip demand remains robust. The reaction suggests investors view TSMC’s capital commitment as evidence that AI infrastructure spending represents structural investment rather than speculative excess approaching correction.

Whether this confidence proves justified depends on whether AI applications develop quickly enough to utilize the infrastructure being built. Training large language models requires massive compute but happens intermittently. Inference—running models to generate responses—occurs continuously but at lower computational intensity per query. If inference volumes don’t scale as rapidly as infrastructure deployment, utilization rates could disappoint even if chip supply eventually meets demand.

TSMC’s planning assumes AI penetration expands from data centers to edge devices, consumer electronics, automotive systems, and industrial applications. Wei noted that AI is starting to grow into daily life, suggesting the company sees demand broadening beyond hyperscaler data centers to distributed computing across multiple form factors and use cases.

The 2-nanometer technology entering production represents a critical inflection point. At 2-nanometer and below, traditional scaling approaches face physical limitations from quantum effects, power density constraints, and manufacturing complexity. Industry roadmaps increasingly incorporate chiplet architectures, new transistor structures like gate-all-around field-effect transistors, and heterogeneous integration of compute, memory, and specialty functions rather than relying solely on planar scaling.

TSMC’s investment in advanced packaging positions the company to capture value as the industry transitions toward these architectural approaches. Packaging technologies like chip-on-wafer-on-substrate and hybrid bonding enable dense interconnects between chiplets that approach on-die bandwidth while maintaining yield benefits from smaller die sizes. These capabilities become more valuable as monolithic scaling economics deteriorate.

The fabrication timeline disconnect—spending capital in 2026 for capacity that contributes in 2028—creates execution risk. If AI demand plateaus or contracts during the interim, TSMC will face capacity additions arriving into a weaker market. The company’s commentary suggests it views this risk as acceptable given the magnitude of long-term opportunity and the competitive positioning benefits from maintaining technology leadership.

For customers, persistent supply constraints through 2027 mean continued competition for leading-edge capacity allocation. Hyperscalers with committed volume purchasing agreements will secure priority access while smaller players face availability challenges and potentially unfavorable pricing. This dynamic reinforces the advantages of scale in AI infrastructure deployment and could accelerate consolidation as companies without guaranteed chip supply struggle to compete.

The $56 billion capex figure represents approximately 37 percent of TSMC’s projected 2026 revenue at the midpoint of guidance. This reinvestment rate far exceeds typical corporate capital allocation, reflecting the capital-intensive nature of semiconductor manufacturing and the urgency the company perceives in building capacity ahead of demand. Whether this investment delivers shareholder returns depends on pricing discipline, yield execution, and demand materialization across the 2028-2029 timeframe when capacity comes online.

TSMC’s earnings call delivered the semiconductor industry’s most authoritative signal that AI represents structural demand justifying unprecedented capital deployment. The contrast between current supply constraints and multi-year capacity buildout timelines suggests the AI infrastructure cycle has years to run before reaching equilibrium—validating the thesis that artificial intelligence represents a generational technology shift rather than a transient trend.

Related Articles

Sources

Research drawn from TSMC Q4 2025 earnings call transcript, CFO Wendell Huang financial guidance, CEO C.C. Wei strategic commentary, TrendForce semiconductor market analysis, Goldman Sachs data center power demand research, Counterpoint Research AI server forecasts, analyst notes from RBC Capital Markets and BTIG on semiconductor sector outlook, and Energy Information Administration projections on data center electricity consumption.