On June 29, South Korea’s government unveiled an 800 trillion won plan to build four memory fabs in Honam — the industrial sequel to a year in which Samsung Electronics and SK Hynix have risen 179 percent and 307 percent, respectively. The same afternoon, foreign investors net sold 7.76 trillion won on the KOSPI, a single-day record. Of that total, 7.17 trillion won — 92.4 percent — came from those two stocks alone.

Samsung fell nearly 5 percent. SK Hynix slipped as well. Honam construction names hit upper price limits. The KOSPI closed down only 0.2 percent because retail buyers and sector rotation absorbed the shock elsewhere. The story is not that Seoul bet wrong on memory. The story is that the national index has become a derivative of two tickers — and the world’s largest allocators were already overweight before the concrete was poured.

Honam Built, Market Sold

The timing looks contradictory only if you read policy and portfolio mechanics as the same language.

For President Lee Jae Myung, Honam is industrial strategy: double DRAM capacity within five years, decentralize fab geography beyond Yongin and Pyeongtaek, tie regional development to the AI supercycle. For a foreign pension fund running a 60/40 with a Korea sleeve, the same headlines raise a different question: how much more semiconductor concentration can one index tolerate?

Securities firms largely described the June selling as profit-taking and half-year rebalancing, not a fundamental rejection of HBM demand. Foreigners had net sold 44.71 trillion won in May and surpassed that figure again through late June. All twenty of the largest single-day foreign net sales on the KOSPI since 1998 have occurred in 2026. Yet when the Honam memoranda were signed, Samsung and SK Hynix still fell — because the buyers at the groundbreaking were not the sellers at the close.

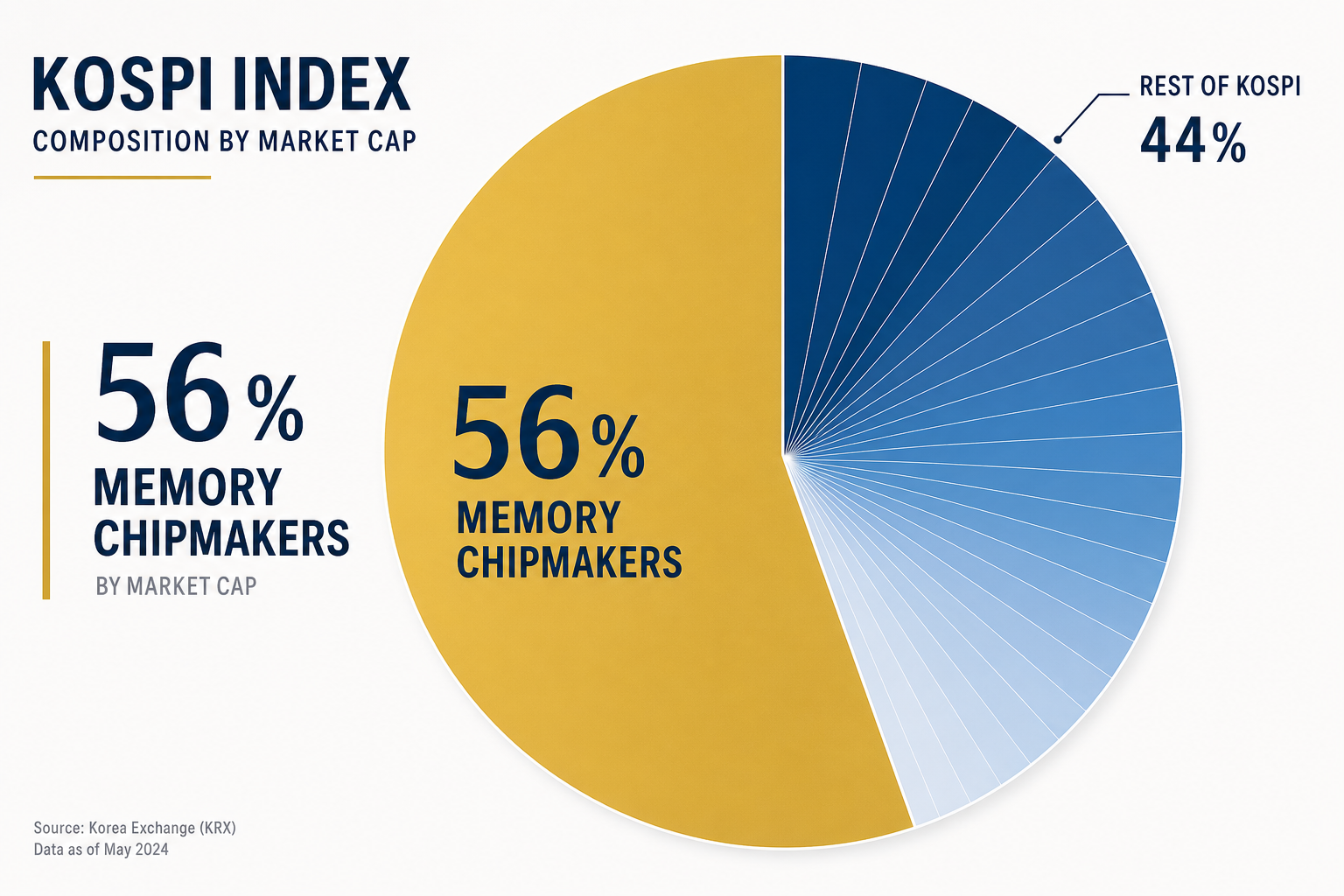

Fifty-Six Percent of a Country

As of late June, Samsung Electronics and SK Hynix together accounted for roughly 56 percent of KOSPI market capitalization — SK Hynix near 28 percent, Samsung near 28 percent, with preferred shares pushing the combined figure toward 58 percent. The weight crossed 50 percent for the first time only in late May. SK Hynix passed Samsung as Korea’s most valuable listed company on June 22 — the first leadership change in twenty-six years.

NH Investment & Securities compared the dynamic to the Magnificent Seven phase in U.S. markets: concentration persists until earnings momentum breaks, not when valuation feels stretched. The difference is depth. America’s top seven names never exceeded half the S&P 500. Korea’s top two already do — in a sector with a documented boom-bust chromosome.

If HBM demand compounds, concentration deepens. If memory pricing stalls, the 44 percent of the index that is not Samsung or SK Hynix cannot cushion the drawdown. KOSPI is not diversified exposure to Korean industry. It is leveraged exposure to DRAM contract curves, Korean industrial policy, and whatever Nvidia’s next accelerator needs stacked underneath it.

Amplifiers, Not Causes

Foreign pension rebalancing explains the scale of June outflows. It does not explain the violence of intraday moves.

On May 27, Korea launched single-stock leveraged ETFs tied to Samsung and SK Hynix. Within a month, net assets in those products grew from 5 trillion won to 17.6 trillion won. On June 26, single-stock leverage ETFs accounted for 35 percent of total ETF turnover — and the KOSPI triggered a circuit breaker for the fifth time this year alone. VKOSPI, Korea’s volatility gauge, touched 97.78, its highest level since the global financial crisis.

The mechanism is short gamma. Leveraged ETFs rebalance into the close to maintain daily 2x exposure — buying more as prices rise, selling more as prices fall. That is not speculation about DRAM’s death. It is mechanical convexity layered atop an index already dominated by two names. Financial Supervisory Service chief Lee Chan-jin expressed regret over the products; the Board of Audit and Inspection opened a review. The ETFs did not cause foreign selling. They turned a concentrated index into a concentrated index with afterburners.

Who Wins, Who Loses, What to Watch

Winners: Direct holders of Samsung or SK Hynix with multi-year horizons and tolerance for 30 percent intraday air pockets. Long-term supply agreements — Micron’s $100 billion in strategic customer contracts through 2030; similar mid-term volume commitments at Samsung and SK Hynix — reduce spot-price exposure for the companies even as index investors feel every tick.

Losers: KOSPI ETF holders who believed they owned Korea Inc. Leveraged and inverse products that compound rebalance drag. Foreign allocators forced to trim winners to preserve geographic diversification — selling into retail bid on the way down.

Watch list:

- July 7: Samsung’s preliminary Q2 2026 guidance — consensus operating profit near 86 trillion won validates the supercycle; a miss revives peak-demand narratives.

- July 10: SK Hynix ADR listing on Nasdaq — potential valuation re-rating or fresh foreign-flow volatility.

- July 23–29: SK Hynix full Q2 results and hyperscaler earnings — Alphabet, Meta, Amazon capex guides dictate whether AI memory demand accelerates into 2027.

- DRAM contract prices for Q3: Flat-to-up would extend pricing power; deceleration is the first crack in the bull case.

Industry estimates put Q2 conventional DRAM contract prices up 58 to 63 percent quarter-on-quarter; mobile LPDDR even higher. Micron’s March-May quarter showed how extreme the current leg can get — revenue up 346 percent year-on-year, operating margin above 80 percent. That is the backdrop against which Honam was announced. The market sold anyway.

The 2027 Cliff

Honam’s first fabs target initial operations around 2028. The nearer cliff is 2027 — when accelerated Yongin and Pyeongtaek capacity meets a memory price curve that may be rising more slowly than in 2026.

If hyperscaler capex guides soften in July, foreign rebalancing will look prescient rather than mechanical. If Q2 prints confirm Micron’s tightness thesis, the concentration trap tightens: more index weight, more ETF amplification, more foreign selling at the highs. Seoul will have doubled down on supply into a market that prices capacity additions as margin risk.

The Honam gamble — the industrial bet — assumes HBM demand is a lamppost. The KOSPI concentration trap assumes the index cannot tell the difference between a lamppost and a flare until the afterburners cool. Gwangju pours concrete. The tape prices concentration. Until July’s earnings, those are the only two stories that matter.

Tags

Related Articles

Sources

Chosun Ilbo and Herald Business on June 29 record foreign selling; Seoul Economic Daily on KOSPI circuit breaker and 56% concentration; Aju Press on single-stock leverage ETFs and VKOSPI; Clarqo and BigGo Finance on index weights; Korea Times and Korea Invest Insights on Q2 earnings calendar and DRAM contract price estimates; CNBC on Honam announcement market reaction