Kevin Warsh assumed the Fed chair in May with a reputation forged in crisis hawkishness. His June inaugural FOMC meeting was deliberately austere: forward guidance deleted, five internal task forces launched, and a press conference that said less than the dot plot. The median projection now sits at 3.8 percent — effectively one hike from the current 3.5–3.75 percent band. Nine of nineteen officials see at least one 2026 increase. Markets heard the numbers and ran: September hike probability sits near 62 percent.

July is when abstraction becomes data.

Sintra Before Payrolls — and That Order Matters

The ECB Forum at Sintra opens July 1 with Warsh on the marquee stage — a day before June nonfarm payrolls land, delayed by the holiday calendar. Consensus expects roughly 172,000 new jobs and 4.3 percent unemployment. Warsh speaks without the month’s defining labor print. Markets will test every word against Thursday’s number.

This is the trap. Hawkish Sintra rhetoric plus a robust payroll report locks September hike pricing near 70 percent and extends the tech-duration selloff. A soft print forces a choice: hold the dot plot’s line, or reveal a chair more data-dependent than his reputation suggests.

June’s correction priced a Warsh Fed markets anticipated. This week prices the inaugural-chair reaction function under live data.

The Inflation Mix Warsh Cannot Ignore

Headline CPI remains above 4 percent, but the composition has shifted. Energy shocks from the Iran conflict are fading: Brent crude sits near $73, removing the gasoline impulse that dominated spring prints. What does not fade is the AI capex bill — data-center electricity, contracted memory scarcity, and semiconductor pricing that Micron’s 81 percent margins exemplify.

Kashkari, Williams, and Barr have framed hyperscaler buildouts as inflationary, not productivity-driven disinflation. The BIS warned the same week that disappointing AI returns could trigger capital withdrawals — but until that reckoning arrives, the spending is real and the CPI line items are arriving at checkout.

Warsh’s trap is intellectual: call AI capex transient and you contradict your committee’s projections; call it structural and you justify the hike bias while growth slows.

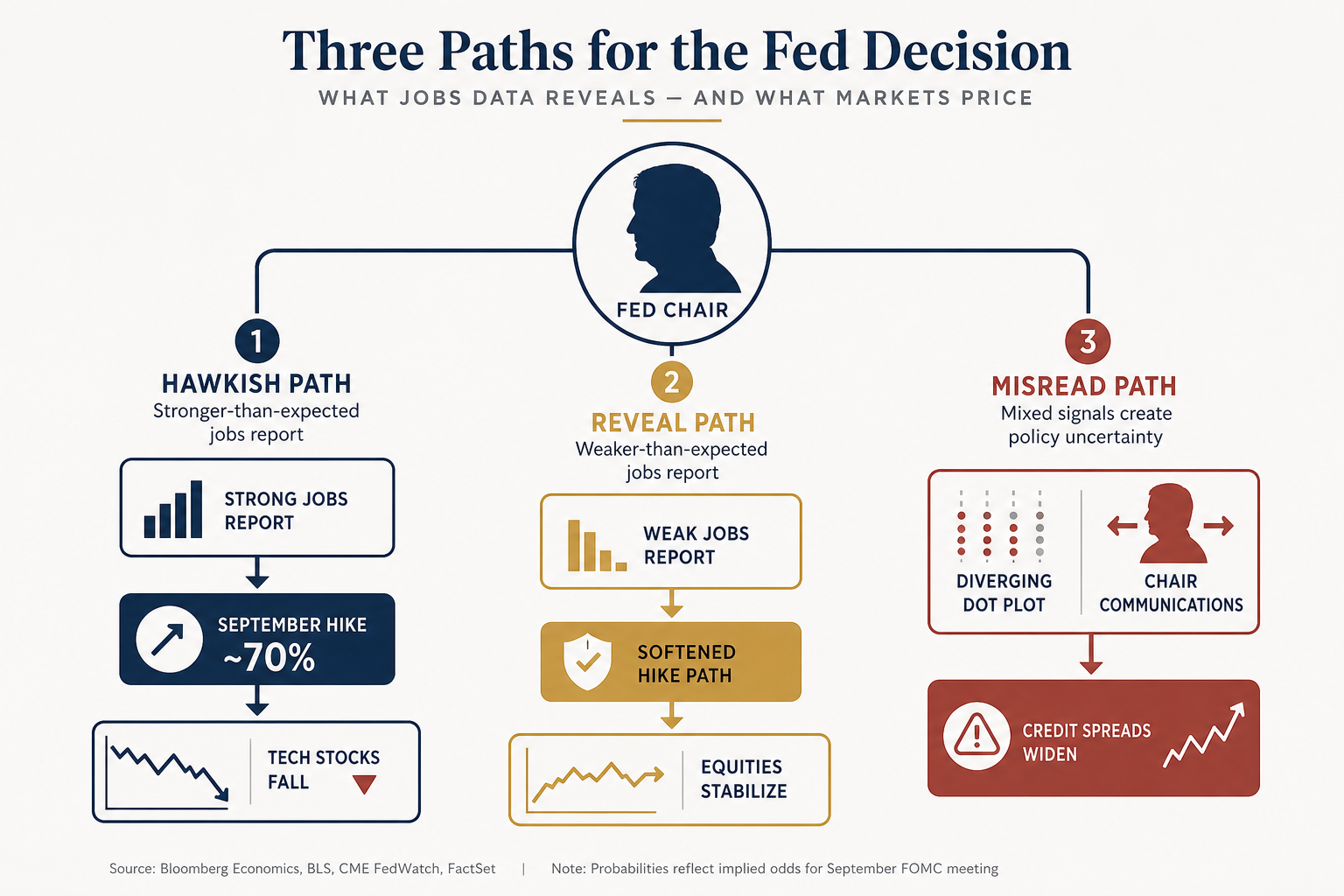

Three Branches From Here

Hawkish confirmation: Strong NFP plus firm Sintra pushes September hike pricing above 70 percent. Duration assets sell; defensives outperform.

The reveal: Weak payrolls — below 120,000 or rising unemployment — force softer Fed communication despite Sintra’s tone. Late-2026 cut pricing re-emerges.

The misread: Dovish Sintra surprise with strong jobs creates dot-plot divergence. Credit spreads widen fast.

What Markets Are Actually Pricing

Fed funds futures bet on a composition story: energy disinflation exhausted, AI input costs persistent, and a chair who deleted forward guidance with nothing soft to deploy.

The July reckoning is less about hawk versus dove than whether markets assigned a reaction function Warsh has not yet demonstrated. The dot plot was the committee’s vote. Sintra is his voice. Payrolls are the economy’s veto.

If all three align hawkish, September is the base case. If jobs weaken, the trap springs — and an inaugural dot plot written before the first major print proves provisional, like most Fed guidance ever was.

Tags

Sources

Analysis based on June 2026 FOMC decision and dot plot, ECB Sintra Forum schedule, delayed BLS payroll release calendar, Fed funds futures pricing, headline CPI composition data, Brent crude levels, and BIS/Kashkari remarks on AI data-center inflation