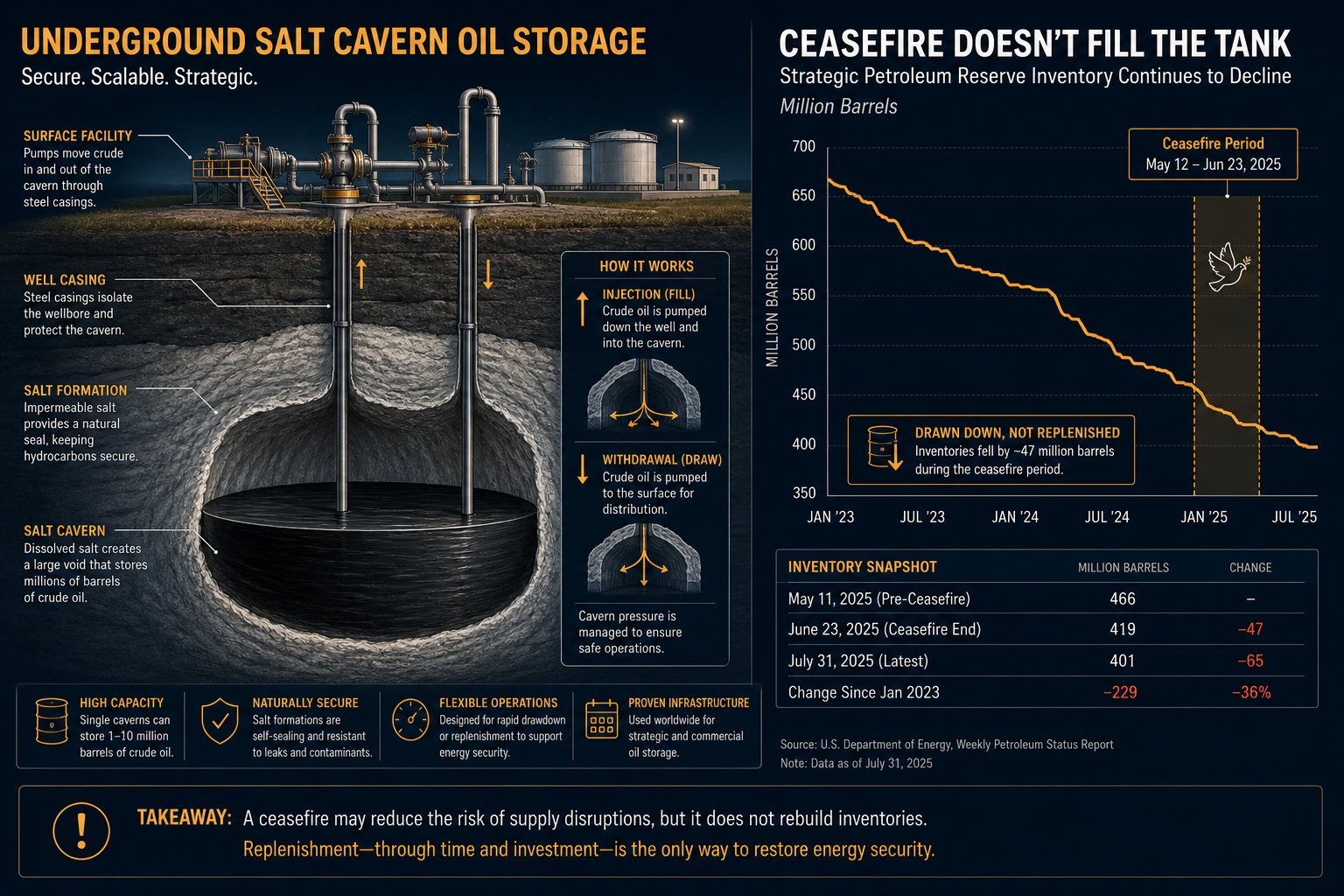

America’s emergency oil cushion has reached the floor of living memory. Department of Energy data for the week ending July 3 show the Strategic Petroleum Reserve at 319.5 million barrels — down 6.2 million on the week and the lowest reading since April 1983. The draw did not pause when diplomacy briefly reopened Hormuz. It accelerated through the ceasefire window traders mistook for recovery.

The binding constraint is no longer price. It is barrels on hand. Since the U.S.–Israeli campaign against Iran began on February 28, combined U.S. inventories have fallen by 120.71 million barrels to 734 million — the lowest aggregate since 1984. Washington released crude to plug a wartime gap. The gap remains. The vault does not.

The 172-Million-Barrel Gamble

In March, Trump authorized a 172-million-barrel SPR release as part of a 400-million-barrel International Energy Agency package. Energy Secretary Chris Wright framed it as a swap: traders take barrels now, return them later with premiums. Salt-cavern discharge rates cap daily outflows at a few million barrels; the initial tranche approaches exhaustion just as geopolitics turns hostile again.

The reserve holds roughly 44.7 percent of its 714-million-barrel authorized capacity. Statutory guardrails matter: limited drawdown authority under the Energy Policy and Conservation Act cannot be invoked below 252.4 million barrels. That floor leaves a margin of about 67 million barrels — uncomfortably thin if Hormuz throughput collapses a second time and the administration faces pressure for another release while markets are already repricing war risk.

Cushing as the Tripwire

If the SPR is the nation’s rainy-day fund, Cushing, Oklahoma is the checking account that sets the price on every screen. The hub — delivery point for West Texas Intermediate futures — rebounded by roughly 700,000 barrels last week but remains below 20 million barrels, a threshold analysts describe as operational stress: below that level, pipeline operators struggle to maintain outbound flow to refineries across the Midwest and Gulf Coast.

Cushing and the SPR are draining in tandem, which is the dangerous part. Emergency releases can mask commercial tightness for weeks. They cannot manufacture storage geometry. When both layers thin simultaneously, the market loses its shock absorber twice — no government barrel to release, no commercial buffer to arbitrage the spike. Andy Lipow of Lipow Oil Associates estimates only about 200 million barrels escaped Hormuz during three weeks of partial reopening — roughly two days of global demand, with perhaps 60 million barrels of that Iranian crude re-sanctioned by Tuesday’s Treasury action.

Hoover on the Horizon

President Trump understands the political economy of empty tanks. At the G7 in late June, he warned that prolonging the Hormuz crisis risked “economic catastrophe” and comparisons to Herbert Hoover — the president who presided over the Depression’s opening act. The line was not rhetorical excess. Low inventories amplify every supply disruption into a gasoline-price headline. Midterm arithmetic does not forgive pump pain financed by visible reserve depletion.

Wednesday’s tape tested the warning. Trump declared the June memorandum of understanding with Iran “over” after fresh strikes on shipping and U.S. bases in the Gulf. Brent climbed toward $78 — not wartime peaks above $120, but enough to push the 10-year Treasury yield to 4.57 percent, its highest since late May. Bond markets, not equity indices, registered the inventory anxiety first. Trump has shown he listens when yields turn “yippy.”

Refill Promises, Empty Caverns

The administration promises to replace drawn barrels — roughly 200 million within a year via swap obligations. Refilling to maximum capacity could cost near $20 billion and take years. Promises are balance-sheet entries. Caverns are geology. You cannot restock a reserve while the strait supplying a fifth of global oil remains a shooting gallery.

Tanker traffic through Hormuz continued Wednesday at roughly a third of normal, according to market sources — even after vessels turned back mid-transit. War-risk premiums for strait transits run $8 million to $10 million per voyage versus $4 million to $5 million for routes outside the chokepoint. Insurance is available; certainty is not. Each transit is a bet that today’s exchange of fire stays bounded. The SPR bet is that it does not.

Final Compression

The SPR bottom is not a data point. It is a policy confession: America spent its emergency oil during a war that paused but did not end. Cushing’s stress level translates that confession into daily pricing. If Hormuz closes again — and Wednesday’s rhetoric makes that the base case to hedge — Washington faces a trilemma: authorize another drawdown toward statutory minimums, accept pump-price political damage, or negotiate under inventory duress. The reserve was built for supply shocks. It was not built to be emptied during a shock that outlasts the diplomacy meant to end it. Watch the caverns, not the communiqués. When the buffer is gone, every headline is inflation.

Tags

Sources

DOE weekly petroleum status data via Reuters and BOE Report on July 3 SPR level; CNN Business and NBC News on Cushing stress and Trump Hoover warning; Energy.gov on 172M barrel IEA-coordinated release; Semafor on statutory drawdown floors; July 8 reporting on MOU collapse and Hormuz tanker traffic