On July 7, NATO leaders gather in Ankara to sign contracts, not make promises. Mark Rutte has previewed tens of billions of dollars in new procurement deals and a Defence Industry Forum on day one. European allies added $139 billion in core defense investment last year. Rutte calls Ankara “maybe even more important than The Hague” because pledges must become metal.

Metal has a supply chain — and Beijing moved first.

Beijing’s Timed Retaliation

On June 22, China’s Ministry of Commerce added ten American entities to its export control list, barring exports of Chinese dual-use goods to them and prohibiting foreign transfers of Chinese-origin dual-use items their way. The list targets Washington’s reindustrialization bets: drone makers, radar firms, Oshkosh Defense, Ball Aerospace — and MP Materials and USA Rare Earth.

Days earlier, the Pentagon blacklisted Alibaba, Baidu, BYD, and other Chinese firms as military-linked. Beijing’s answer was calibrated: not a blanket embargo, but a signal aimed at the two firms building America’s mine-to-magnet pipeline. MP Materials runs the Mountain Pass mine in California with Pentagon backing. USA Rare Earth, in which Washington took a 10% stake in January under a $1.6 billion package, is opening an Oklahoma magnet plant later in 2026.

Analysts call the curbs largely symbolic — both firms say they have cut Chinese dependence. In export-control diplomacy, symbolism is the point.

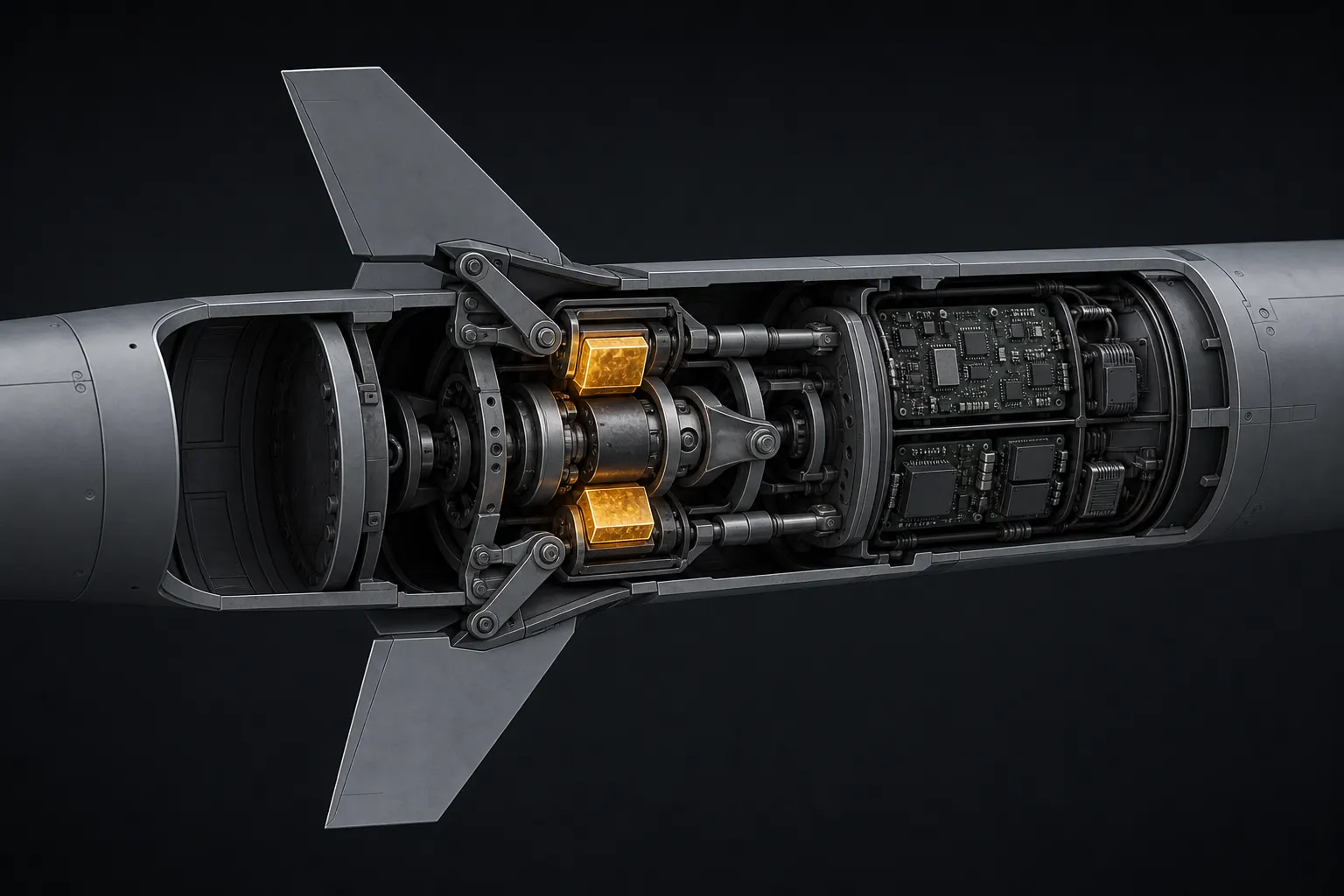

The Magnet Inside the Missile

Permanent magnets are flight-critical, not commodity. Storm Shadow cruise missiles use samarium-cobalt actuators because they perform above 150°C, where neodymium degrades. Patriot guidance assemblies, THAAD gimbals, and NATO radar fire-control systems depend on the same materials.

NATO listed twelve defense-critical minerals in 2024; rare earths appear in nearly every platform. China controls separation, metallization, and finished magnet production — roughly 90% of global processing. This is weaponized interdependence one layer below semiconductors: chip controls throttle compute; magnet controls throttle guidance.

MOFCOM 61 and the 0.1% Rule

The entity list builds on MOFCOM Announcement No. 61, effective December 1, 2025, which asserts extraterritorial control over foreign-made magnets containing as little as 0.1% Chinese-origin rare-earth content by value — plus products made abroad using Chinese processing technology. Military end-user licenses are, in principle, denied.

The G7 answered at Evian on June 17, pledging no single non-G7 supplier would exceed 60% of rare-earth and magnet imports by 2030. For processed magnets, where China’s share nears 90%, analysts call that target aspirational. Lynas shelved a Pentagon-funded Texas facility; USA Rare Earth faces a technology lawsuit. The G7 cited €64 billion across 195 projects since January. Announcing is not refining.

What Ankara Can and Cannot Deliver

Rutte’s agenda is contracts, production floors, Ukraine financing, and Hormuz language. The Defence Industry Forum will feature MOUs and pre-packaged procurement designed to signal resolve.

What a summit cannot manufacture is certified non-Chinese magnet capacity at scale. DFARS 252.225-7052 bars Chinese-origin magnets in qualifying U.S. defense systems from January 1, 2027 — six months after Ankara. Pentagon DPA funding is scaling domestic producers, but capacity cannot yet absorb simultaneous Patriot replenishment, Storm Shadow resupply, and Rutte’s production ramp.

Ukraine makes the tension visible. After a June 29 barrage that killed an F-16 pilot, Zelenskyy is ready to buy Patriots. Every interceptor draws down stockpiles whose guidance subsystems trace to the magnet chain Beijing is contesting.

The Countdown to July 7

The acute story is calendar collision. Ankara convenes in seven days. Beijing’s entity list landed eight days ago. The DFARS deadline arrives in 185 days. G7 diversification targets stretch to 2030. NATO’s joint stockpiling initiative — agreed by twelve allies in 2025 — is the right response. Institutions move slower than export-control notices.

For investors, Ankara is a sentiment event with a materials-science footnote. Contract announcements will move defense primes. The binding constraint will not appear in the communiqué. It lives in Oklahoma magnet plants, Mountain Pass separation lines, and MOFCOM license queues.

The alliance can pledge production at scale. Steering at supersonic speed still runs through Beijing’s refining architecture until allied mine-to-magnet capacity clears the DFARS cliff. Ankara will showcase the contracts. The chokehold arrives on the bill of materials.

Tags

Sources

NATO summit overview, POLITICO and Anadolu Agency on Ankara contracts, China Ministry of Commerce June 22 export control list, Bloomberg and Al Jazeera on entity-list retaliation, G7 Evian critical minerals declaration, Jones Day and CSET on MOFCOM Announcement 61, MBDA and RUSI supply-chain analysis, DFARS 252.225-7052 defense sourcing deadline