While countries push out tax and oil relief, China pushes out a brand new cruise ship.

On Friday morning in Shanghai, tugboats guided the Adora Flora City out of its construction dock at Waigaoqiao Shipbuilding — a 141,900-tonne vessel, 341 meters long, fitted with 2,130 cabins, 26 restaurants, and an AI-integrated entertainment suite. It is China’s second domestically built large cruise liner, delivered just two years after the first, and it is already 17 meters longer and 7,000 tonnes heavier than its predecessor. Sea trials begin in May. The third ship is planned for 2030, this time fully designed in-house.

The timing is almost satirical. The same week, the United States crossed $39 trillion in national debt, the Federal Reserve held rates while admitting inflation is not coming down as hoped, and the White House waived the Jones Act — a century-old shipping law — for 60 days in a scramble to move oil between domestic ports while Iran chokes the Strait of Hormuz. One country is building the crown jewel of civilian shipbuilding. The other is suspending its own maritime rules to keep gas flowing.

Together, those snapshots suggest the U.S. economic outlook is considerably murkier than equity markets imply.

Gold Is Not Just Rising — It Is Screaming

Gold began March above $5,400 an ounce. It has since swung violently — touching $5,114 mid-month before crashing to $4,551 and recovering to $4,660 on Friday — but the trend remains staggering: the metal is up more than $1,600 from a year ago, a gain exceeding 50% in twelve months. Central bank demand remains the structural floor. The People’s Bank of China extended its gold purchases for a fifteenth consecutive month in January, and J.P. Morgan projects global central bank and investor demand will average 585 tonnes per quarter through 2026.

The volatility, not just the direction, matters. Gold swinging $700 in a week is not a commodity finding its price. It is capital looking for cover and finding the room crowded. When the traditional safe haven becomes itself a source of risk, it signals that the market’s model for pricing dollar-denominated stability is breaking down. China’s central bank knows this. Fifteen months of buying is not a trade. It is a reallocation thesis.

Semiconductors: The AI Bid Meets a Technical Ceiling

The Philadelphia Semiconductor Index peaked at 8,498 on February 25 and has since retreated to around 7,863 — a decline of roughly 7.5% in three weeks. The iShares Semiconductor ETF issued a sell signal from a pivot top in late February and is trading near its 52-week midpoint, with the MACD trending negative. The AI story that powered the sector through 2025 — hyperscaler capital expenditure, GPU demand, advanced packaging tightness — has not disappeared. But the bid is narrowing.

Beijing offers a sharp contrast here. It is not playing the same semiconductor cycle. It is building the fabrication layer underneath it — investing in domestic chip production capacity while the United States debates export controls and tariff structures. China’s second cruise ship, incidentally, features AI-integrated systems designed and built domestically, a quiet demonstration that the country is moving up the value chain in applied compute, not just theoretical capacity. The American semiconductor trade, by contrast, remains a leveraged bet on a handful of names whose valuations assume perfect execution in an imperfect world.

Treasuries: The Yield Curve Has a Credibility Problem

The 10-year Treasury yield sits at 4.265%, the 2-year at 3.775%, and the 30-year at 4.88%. The Fed held rates on Wednesday and still projects one cut this year, but Chair Powell’s language was blunt: inflation is not receding as the committee had hoped. Producer prices rose 0.7% in February, with core PPI at 0.5% — both well above the 0.3% consensus. The Fed’s own growth forecast for 2026 was slashed to 0.9%.

That combination — sticky inflation, fading growth, and a central bank paralyzed between its dual mandates — is the textbook setup for a credibility problem. The bond market is already showing it. Government bonds’ safe-haven status was openly questioned last week as yields failed to fall meaningfully even as equities sold off and the Iran conflict escalated. When bonds stop behaving like shelter during a geopolitical shock, something foundational has shifted in how the market prices U.S. sovereign risk. Net interest payments on the national debt are projected to exceed $1 trillion this fiscal year — nearly triple what they were in 2020.

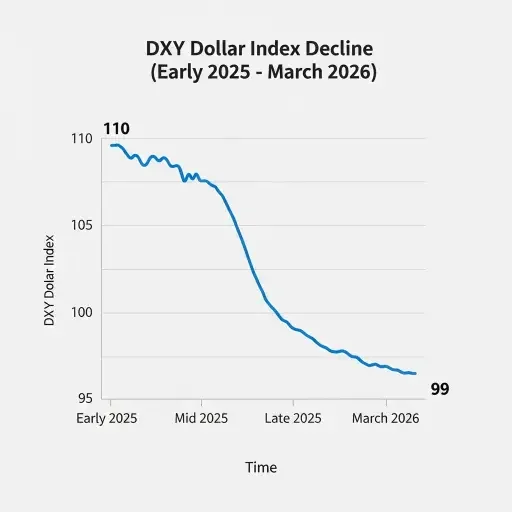

The Dollar Tells the Binding Story

The DXY largely matches what those three markets are signaling. The index has fallen roughly 10% from its January 2025 peak above 110 and currently hovers near 99. The bounce above 100 this week — driven by safe-haven demand from the Iran conflict — looks temporary. Goldman Sachs, Deutsche Bank, and Morgan Stanley all project further weakness through year-end, with targets clustering in the low-to-mid 90s. The structural case is straightforward: narrowing rate differentials, persistent fiscal deficits, and waning confidence in U.S. macroeconomic stewardship. Morningstar notes the dollar remains roughly 15% overvalued relative to major peers on a purchasing power parity basis, even after the selloff.

China, meanwhile, reported cruise tourism throughput up 25% year-on-year in 2025 and is launching international routes from Guangzhou next year. It is not just building ships. It is building demand infrastructure — ports, routes, consumer ecosystems — while the dollar’s custodians manage a war, a debt spiral, and an oil shock simultaneously.

None of this means the U.S. economy is collapsing. It means the signals investors rely on to price the future — the gold premium, the chip multiple, the term premium, the reserve-currency discount — are all moving in the same direction, and that direction is away from confidence. The outlook is not bearish or bullish. It is unsure. And unsure, in a market that has been priced for certainty, is its own kind of risk.

China is building cruise ships. America is waiving shipping laws. The gap shows up first in how gold, semiconductors, Treasuries, and the dollar trade—not in slogans.

Tags

Related Articles

Sources

Market data from Fortune, Trading Economics, TradingView, CNBC, Yahoo Finance. Ship data from Xinhua, CGTN, Marine Insight. Fed commentary from CNBC, Yahoo Finance. Dollar analysis from Cambridge Currencies, Morningstar, OANDA. Fiscal data from CRFB, Peterson Foundation, Fox Business.