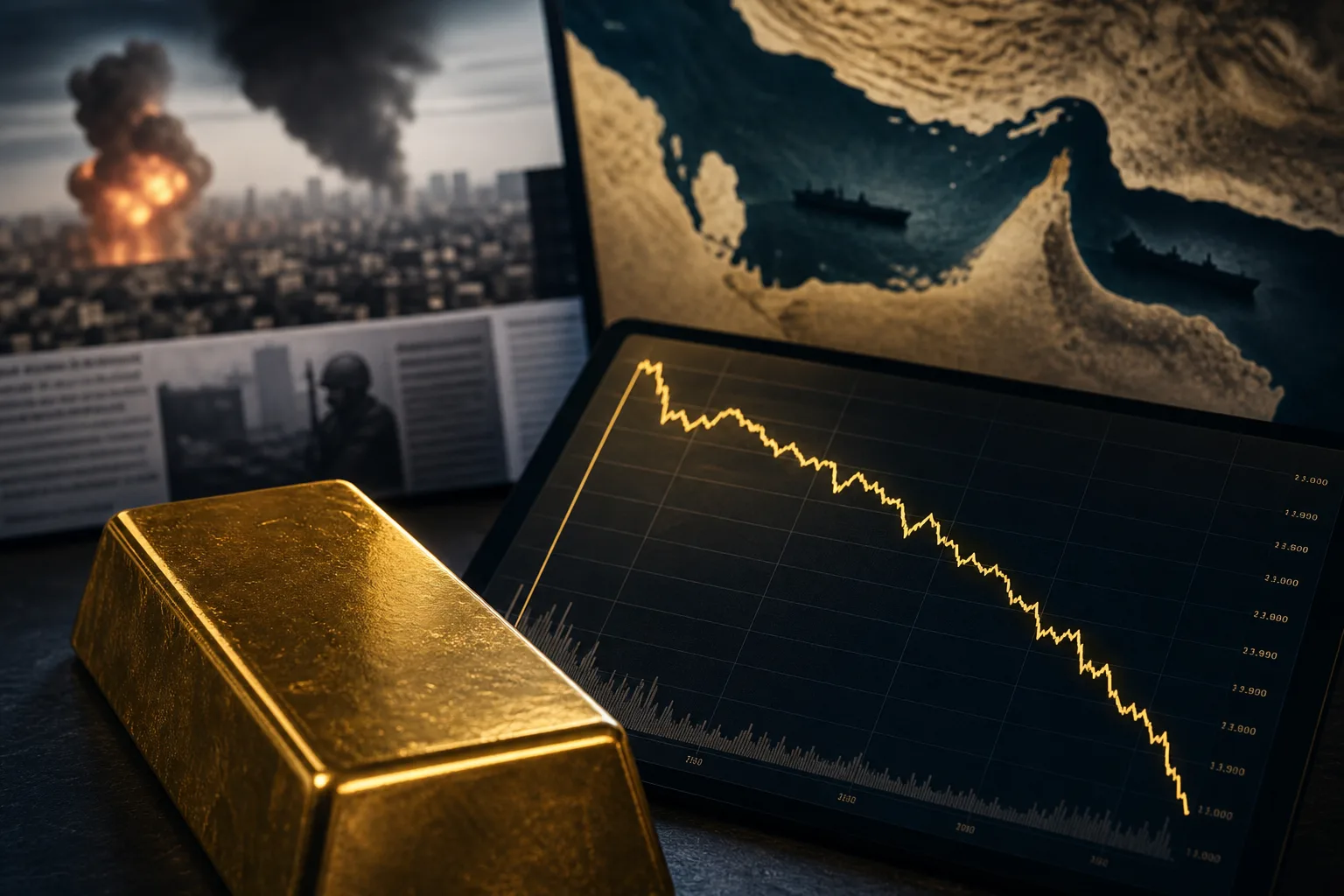

The safe-haven trade broke in February and never rebooted. Gold ripped toward the mid-$5,000s as U.S.–Israeli strikes opened the Iran war, then spent spring and summer surrendering that premium — even as Hormuz stayed contested, the June memorandum frayed, and Sunday’s IRGC closure plus strikes on five Gulf states lit every geopolitical dashboard. Fear still sells. It just no longer clears the opportunity-cost hurdle set by real yields.

The mechanism is almost boring once you see it. Oil lifts near-term inflation. A hawkish Federal Reserve — funds still at 3.50–3.75% under Chair Kevin Warsh — keeps real rates elevated. Gold pays nothing; capital rotates into dollars and Treasuries. That is why the metal could fall more than 20% from its war-onset neighborhood near $5,300 into the low $4,000s, and why last week’s “ceasefire is over” headline pushed Brent higher while gold slid toward $4,050. The war is the input. Rates are the price.

The MoU Break Reopens the Inflation Channel

June’s interim deal was a rates story disguised as diplomacy. Optimism that Hormuz would normalize pulled the oil curve and near-term inflation compensation lower; equities and the dollar firmed. The reverse is now running. War-risk insurance near 5% of vessel value, tanker counts collapsing from seventy-plus daily ceasefire transits toward roughly a dozen, and a third U.S. strike package this week all re-ligate energy to CPI. Brent’s mid-to-high seventies still price residual-barrel comfort; a strait “open” in a presidential interview and closed in an IRGC communiqué is a coin flip with freight attached.

Gold will not automatically catch that flip. It catches the second derivative — whether the Fed reads the oil print as theater or as a hike trigger. June minutes already split the Committee on end-2026 rates. AI infrastructure demand, not only Hormuz, is the other inflation stalker in those minutes.

Three Year-End Regimes for Rates, AI, Chips, and RAM

Scenario A — Contained attrition. Strikes continue, mediators keep a technical channel open, and enough southern-route oil still clears to hold Brent roughly $75–90. The Fed stays on hold. Gold ranges. Hyperscaler capex — already load-bearing at roughly 8% of U.S. GDP and more than a quarter of growth — keeps grinding. HBM and DRAM remain tight on AI allocation, not war. Memory inflation and software bundling still add to core PCE, but the Committee treats chipflation as a supply story it cannot rate away. Equities stay hostage to the AI complex more than to Tehran.

Scenario B — Sustained choke. Hormuz traffic stays near wartime lows for weeks; insurance and dark-fleet friction do what a formal blockade would. Oil pushes toward the mid-nineties or higher. The Fed’s hike faction wins 25 basis points; real yields firm; gold’s first impulse stays down or sideways until growth cracks. AI buildout does not stop — power and chips are strategic — but financing costs rise, marginal data centers slip, and consumer electronics feel the RAM tax harder. Beijing’s capped H200 ration becomes more valuable as Western compute stays expensive.

Scenario C — Credible reopen. An enforced corridor, indemnity, or renewed MoU collapses the war-risk premium. Oil retreats, inflation compensation eases, and gold’s real-yield headwind softens — the late-year path toward $4,500 some houses still sketch. AI and memory stay tight; the Fed can debate cuts without looking reckless. That is the only regime in which February’s promise partially returns without a recession.

What the Tape Is Actually Saying

Sunday did not restore gold’s wartime premium. It confirmed the hierarchy: missiles move oil; oil moves the Fed; the Fed moves gold. Chips and RAM sit in a parallel inflation loop that survives any single ceasefire. The binding constraint is capital’s reading of real yields and AI demand — not the latest communiqué from Bandar Abbas or Ankara. Watch tanker counts, war-risk quotes, and the July 29 FOMC more than the revenge telegram. In this war, the metal that was bought for fear is still being sold for rates.

Tags

Sources

July 12 Hormuz closure and Gulf strikes reporting; gold path from ~$5,327 war-onset spike to ~$4,000–4,175 by early July; July 8 MoU-over selloff near $4,050; Fed funds 3.50–3.75%, June minutes under Chair Warsh; AI investment ~8% of GDP / >25% of growth; Goldman on memory/software PCE pressure; Lloyd's war-risk ~5% of vessel value