Bitcoin’s market capitalization fluctuates by hundreds of billions on sentiment alone. That volatility tells us little about whether the protocol will function as intended in 2040 or 2140. The relevant question is structural: does the network’s incentive architecture, governance topology, and cryptographic foundation remain viable as subsidies decay, institutions accumulate, and adversarial technology evolves?

We evaluate four vectors — economic security, game-theoretic co-optation, cryptographic obsolescence, and Layer-2 dependency — and ask whether empirical data supports systemic obsolescence or an institutional equilibrium shift.

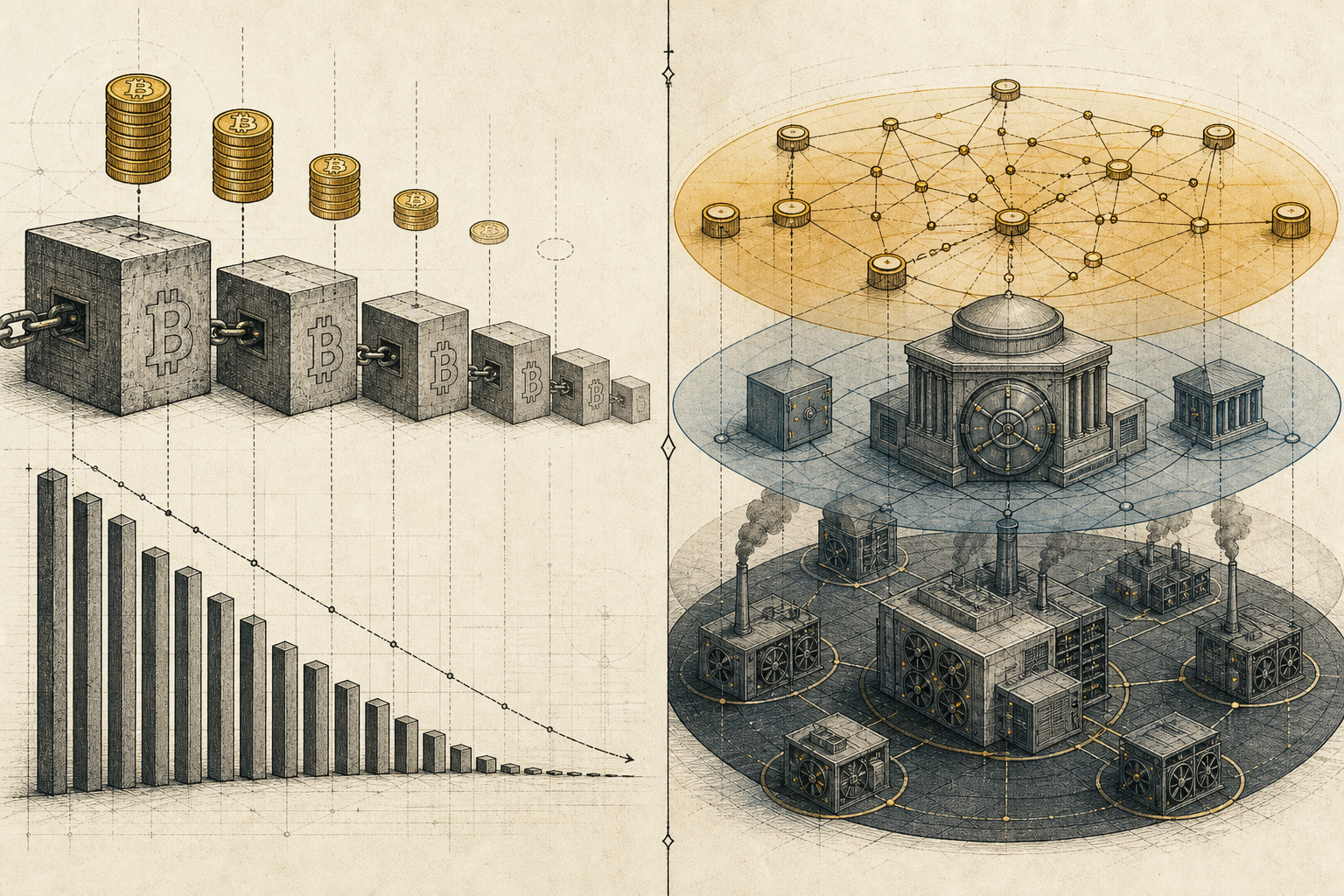

Vector I: The Security Budget and the Fee-Only Future

Proof-of-work security is a pricing problem. Honest miners extend the chain because block rewards exceed their costs; attackers must outspend that aggregate to reorganize history. Today, the block subsidy stands at 3.125 BTC per block following the April 2024 halving. Transaction fees contribute roughly 5–15% of total miner revenue in normal conditions — higher during congestion events (Ordinals waves, fee spikes), lower in quiet periods.

The asymptotic schedule is fixed: subsidy reaches zero around block 6,930,000 (~2140). After that, security depends entirely on fee revenue. The sufficiency debate splits cleanly. Optimists cite Satoshi’s original design — growing settlement demand multiplied by scarce block space should fund adequate hash rate — and point to post-halving hash rate growth as evidence the market adapts. Skeptics invoke Carlsten et al.’s “fee-sniping” model: in a pure fee market, high variance between blocks incentivizes miners to fork recent blocks rather than extend the tip, creating instability that undermines Byzantine fault tolerance.

The near-term data neither confirms crisis nor resolves the debate. Hash rate reached record levels after the 2024 halving. Public miners sold record volumes in Q1 2026 when prices softened, but hashprice recovered above breakeven as BTC rebounded. The 2028 halving — subsidy falling to 1.5625 BTC — is the next empirical test.

Macroeconomic conditions that would threaten BFT: sustained low on-chain demand combined with falling nominal BTC price, compressing fee revenue while fixed energy costs rise. That produces miner capitulation, hash rate decline, and a lower cost of 51% attack — a tragedy-of-the-commons spiral if settlement value on-chain shrinks faster than off-chain demand can backstop periodic high-fee anchors. Conversely, if Bitcoin functions primarily as a macro reserve asset with intermittent high-value settlement (ETF rebalancing, treasury movements, Lightning channel opens), fee spikes may suffice. The security budget is not failing today. It is unproven at scale on a fee-only basis.

Vector II: Financialization and the Censorship-Resistance Thesis

Bitcoin’s political promise was permissionless transfer. Institutional financialization tests that promise at two layers: custody and block production.

U.S. spot Bitcoin ETFs collectively hold approximately 1.3 million BTC — roughly 6.5% of circulating supply — with BlackRock’s IBIT alone controlling over 813,000 BTC. Coinbase Custody holds an estimated 84% of ETF assets. This is not on-chain concentration; it is off-chain settlement risk. ETF shareholders do not control keys. Redemption flows, regulatory actions, or custodial failure propagate through a single operational node.

Mining presents a parallel topology. Foundry USA and AntPool together account for roughly half of observed block production; four pools control 70–75%. Pool operators coordinate transaction selection — a soft form of censorship. Oman nationalized licensed hashrate through a state-mandated pool in June 2026, demonstrating that sovereign actors can convert pool choice from market decision to compliance obligation.

Does this constitute existential governance capture? Not yet in the protocol sense. Bitcoin’s consensus rules remain unchanged by ETF inflows. No institution can inflate supply or rewrite history without hash rate. But the practical censorship-resistance thesis erodes: if most economic Bitcoin lives in custodial wrappers and most blocks are assembled by a handful of pools, the user experience of “Bitcoin” becomes indistinguishable from regulated financial infrastructure with a proof-of-work appendix.

Stratum V2 adoption — with major pools enabling miners to construct their own block templates — is a countervailing force. The June 2026 DMND block mined via Stratum V2 Job Declaration suggests template sovereignty can decentralize at the margin. The equilibrium is bifurcated: base-layer rules remain resistant; economic and political layers increasingly resemble traditional finance.

Vector III: Cryptographic Obsolescence and Governance Inertia

SHA-256 proof-of-work is not the near-term vulnerability. ECDSA and Schnorr signatures on secp256k1 are. Shor’s algorithm, executed on a cryptographically relevant quantum computer, derives private keys from exposed public keys. Estimates vary — Google researchers have cited timelines as aggressive as 2029 for breaking Bitcoin’s signature scheme; NIST’s broader migration horizon extends to 2035.

The exposure is not hypothetical in inventory terms. An estimated 6.5–6.9 million BTC sit in addresses with exposed public keys — including long-dormant early-miner UTXOs. BIP-360 (merged February 2026) introduces Pay-to-Merkle-Root outputs that hide keys pre-spend. BIP-361 (April 2026) proposes a phased sunset of legacy signatures with rescue protocols for legitimate holders.

Bitcoin’s hard-fork aversion — historically a feature — becomes a liability in compressed migration windows. Soft-fork upgrades require overwhelming coordination; contentious sunset proposals risk chain splits. Social inertia protects stability until it prevents adaptation. No quantum machine threatens the network today. The risk is timing mismatch: if CRQC arrives before migration completes, exposed UTXOs become a bank run executed by physics rather than psychology.

Governance is responding, but slowly relative to institutional threat models. The protocol is not incapable of upgrade — Taproot activated in 2021 — but quantum migration is orders of magnitude more disruptive than prior forks. Cryptographic obsolescence is a tail risk with binary payoff, not a gradual decline.

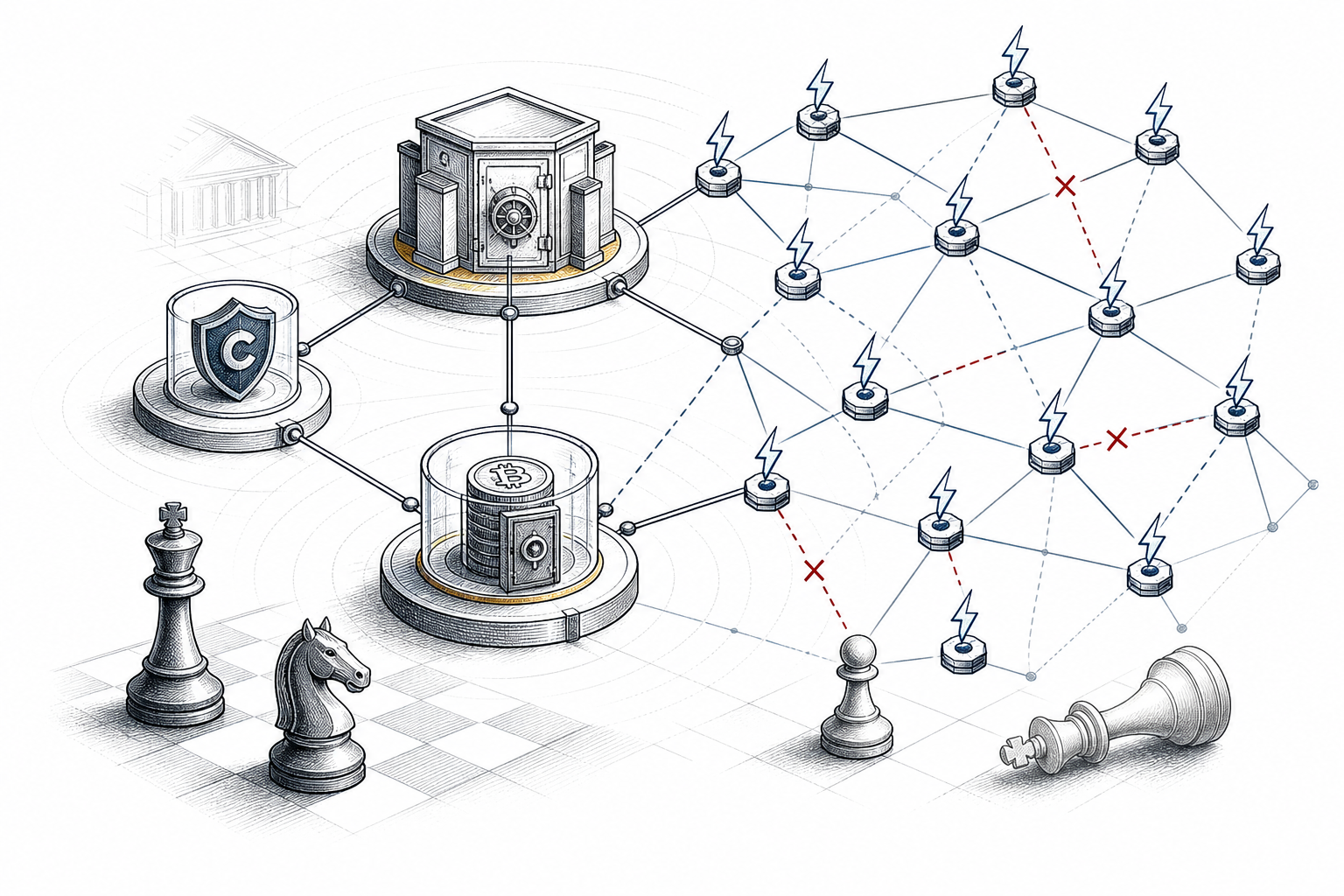

Vector IV: Layer-2 Dependency and Base-Layer Throughput

Bitcoin L1 processes roughly seven transactions per second. Sovereign monetary function at scale requires either L2 velocity or acceptance of L1 as a low-frequency settlement rail — the gold-standard model.

Lightning Network public capacity holds approximately 4,900 BTC across ~41,000 channels (May 2026), down from a December 2025 peak of 5,637 BTC. Monthly routed volume exceeded $1.17 billion in late 2025 — a 266% year-over-year increase — driven partly by exchange integrations (Coinbase, Binance, OKX). Yet node counts fell from a 2022 peak of ~20,700 to ~17,400, suggesting consolidation rather than organic mesh expansion.

Lightning’s constraints are structural: inbound liquidity requirements, online recipients, routing failures, and force-close costs during high-fee periods. Liquid, Ark, Spark, and statechain architectures offer alternative trust models — some federated, some channelless — trading purity for usability.

If L2 ecosystems fail to achieve self-sustaining velocity, L1 alone cannot support retail monetary throughput. It can, however, function as a finality layer for high-value settlement — ETF flows, treasury movements, inter-exchange net settlement — with L2 handling retail payments where adoption succeeds. The dichotomy is false binary: L1 does not need Visa-scale throughput to survive as a settlement engine. It does need L2 or periodic L1 demand sufficient to fund the security budget. Current data shows L2 growth in volume but concentration in infrastructure — not failure, not triumph.

Synthesis: Terminal Decline or Institutional Equilibrium?

Empirical signs do not support terminal structural decline in 2026. Hash rate is at historic highs. ETF inflows represent demand-side validation, not protocol compromise. Developer activity on quantum migration is accelerating. Lightning volume grows even as node topology consolidates.

What the data supports is an institutional equilibrium shift: Bitcoin evolving from cypherpunk peer-to-peer cash toward a stratified stack — regulated custody for most holders, pooled mining for block production, L2 rails for payment velocity, L1 for irreversible settlement and supply integrity. Censorship resistance persists in code; censorship susceptibility increases in practice for the median user.

Existential risks remain real but horizon-dependent. Fee-only security is untested at subsidy zero. Quantum migration requires coordination Bitcoin has never attempted at this scale. Custodial concentration creates systemic off-chain nodes that regulation can reach even when the chain cannot.

The network is not dying. It is mutating — and the mutation trades ideological purity for institutional adoption, with long-dated tail risks that price markets largely ignore because they exceed quarterly earnings horizons.

For readers evaluating the thesis of systemic obsolescence: the honest verdict is conditional survival. Bitcoin’s base layer remains the most battle-tested monetary protocol in digital history. Whether it remains the monetary standard its holders assume depends on fee markets that have not yet been tested, cryptography that must migrate within a decade, and a social contract that must tolerate becoming, in practice, what it was designed to replace.

Tags

Sources

Analysis informed by post-2024 halving mining economics, U.S. spot ETF custody disclosures, BIP-360/BIP-361 post-quantum proposals, Lightning Network capacity data, Stratum V2 adoption, and academic work on fee-market security (Carlsten et al.) and mining pool game theory