In the ledger of modern education, Physics Wallah (PW) stands as a paradoxical chassis: a company that sells lectures, yet moves the dull ache of test anxiety into the propulsion of a public-market machine. Its recent IPO, clocking a roughly $5 billion market capitalization, did not merely revalue a startup; it reparameterized the audience for EdTech—students, parents, and even policy wonks—into a single, investable narrative: that scalable learning can be both affordable and profitable. It is an origin story written in balance sheets and syllabi, with a cadence reminiscent of a high-stakes boardroom diary.

PW began by reframing education as a journey with a capitalizable road map: democratized access reached through digital libraries, low-cost content, and exam-cracking coaching. Like a sun-drenched market in a crowded field, it found its edge by aligning pedagogy with the psychology of aspiration. In a country of 1.4 billion minds, the platform’s core proposition—high-quality video lectures, structured test prep, and affordable price points—tapped into a deep-running demand for reliable success signals. The IPO did not appear from nowhere; it was the culmination of a product-market fit that had social velocity and financial gravity.

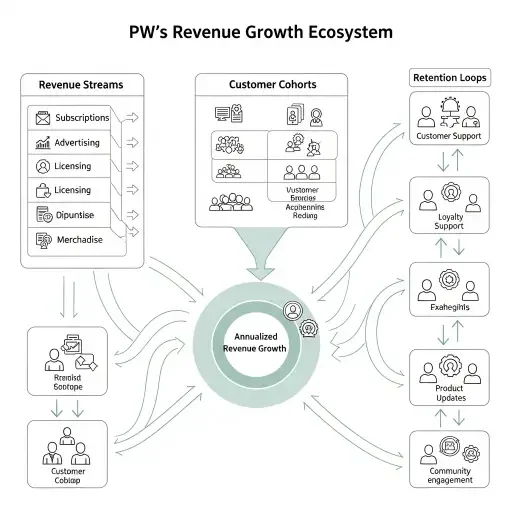

The visual economy of PW’s growth is legible: a blueprint of recurring revenue built on course bundles, subscription tiers, and micro-credentials that promise employability benefits. The company’s moat is not simply brand or content—though those matter—it’s the design of learning as a continuous loop. Students do not just buy a course; they buy a system that maps backlog to breakthroughs, a cognitive scaffold that can transition from a single exam to a portfolio of competencies. This is where the narrative ecology of PW meets the mechanics of market cap: a productized education pipeline, with retention as the revenue engine and completion as a signal to investors of durable demand.

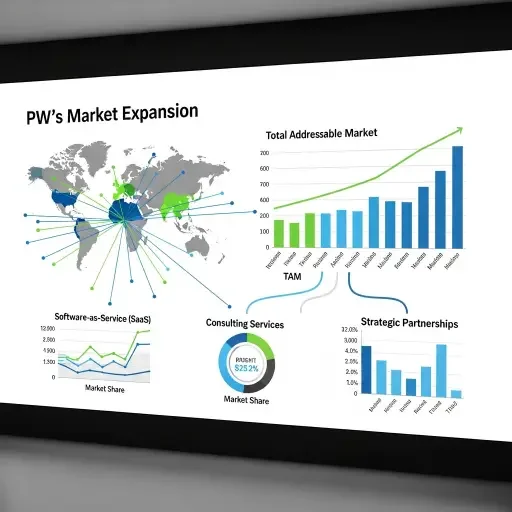

From a governance vantage, PW navigated the typical EdTech crosswinds: price sensitivity, regulatory uncertainty, and the high-beta nature of consumer education. The readiness for an IPO required a clarity around monetization that could withstand scrutiny from analysts, auditors, and the public market’s appetite for risk. The company’s disclosures indicated a plan to scale beyond exam prep into broader lifelong learning, a strategy that reduces single-event dependency and elevates lifetime value (LTV) per user. In this architecture, the IPO is less a bet on a flash-in-the-pan craze than a bet on a durable learning framework with scalable pedagogy and predictable revenue rhythms.

The cognitive architecture of PW’s value proposition also speaks to a broader social calculus. Education, in the PW articulation, is not a zero-sum commodity; it is a winner-take-some architecture where differentiation occurs at the intersection of affordability, quality, and accessibility. If the market is a basin of liquidity, PW’s design steers that liquidity toward a model of ongoing engagement—periodic refreshers, new syllabi aligned to evolving exams, and community-driven content creation that lowers marginal cost of content expansion. For investors, this is the critical signal: the flywheel is not a single product carousel but a system that can churn out updated curricula with minimal disruption to user retention.

Yet the cautionary dial is not silent. The venture beat remains sensitive to user churn, platform competition, and the volatility of consumer spend in education. The $5B valuation rests on a narrative of go-to-market discipline and growth levers that must endure macro headwinds: inflationary pressure on discretionary spending, shifts in education policy, and the competitive intensity from global EdTech accelerators and local upstarts alike. The intellectual discipline for PW is to preserve the cognitive load balance it optimized during launch: keep the learner’s journey predictable enough to prevent cognitive fatigue, yet fresh enough to sustain curiosity and enrollment velocity. In practice, that means disciplined product roadmaps, modular content, and transparent retention metrics that satisfy a market increasingly hungry for data-driven bets.

The strategic spectrum can be summarized in three lines. First, PW’s core artifact—high-quality, scalable content—transforms education into an “always-on” service, which aligns with a subscription economy and recurring revenue expectations. Second, the public market’s extra layer—transparency, auditability, governance—converts the platform’s growth into a tradable asset class, offering risk-adjusted perspectives for institutional investors. Third, the social dimension—that education should be accessible without surrendering quality—anchors a long-run growth thesis, one that contemplates regulatory sensitivity and the aspiration of a billion learners who crave credible pathways to opportunity.

But what of the cognitive economy—the reader’s mental model under pressure? The PW story, when told with an aware rhythm, becomes a map rather than a rumor. The title compresses the entire arc into a seed; the lede sketches the trajectory; paragraphs modulate novelty to keep the mind aligned. The macro-structure keeps returning to one proposition: scalable learning can be a durable, investable system when it maintains clarity, consistency, and compassion for the learner. In the end, the PW IPO is not just a financial milestone; it is a case study in turning education into a sustainable asset class—one that respects the reader’s cognitive tempo as a first principle of design.

Recap in one line: Physics Wallah turned a classroom into a scalable public-scale engine by aligning pedagogy with predictable revenue, investor confidence, and lifelong learning promises.

As a closing visual metaphor, imagine a lecture hall reframed as a grid of dynamic cables—each cohort a conductor, each course a resonance, each revenue stream a current. When tuned correctly, the entire room hums with clarity: a public company that teaches as it trades, and trades as it teaches.

This is not merely a story of an EdTech triumph. It is a primer on how to design information and organization so that the human brain travels further with less friction—and a reminder that the market rewards education when it is engineered with empathy, precision, and relentless iteration.

Tags

Related Articles

Sources

Public market filings, interviews with founders, investor analyses, and education market reports.