The warning came not from a regulator or academic, but from inside the industry itself. Katie Koch's firm manages $433 billion. When she says she's "very nervous," the market should be terrified.

On November 5, 2025, as global markets digested yet another day of volatility, a quiet alarm bell rang from an unexpected quarter. TCW Group Inc., managing some of the world's most sophisticated capital, issued a stark warning about the private credit market—a shadow banking system that has ballooned to $2.1 trillion while operating largely beyond regulatory view.

The timing wasn't coincidental. Just hours earlier, Hong Kong's stock exchange reported a 56% profit surge driven by frenzied trading activity, while global equity markets experienced their second consecutive day of declines amid valuation fears in the technology sector. The divergence revealed something crucial: capital is searching desperately for returns, even as traditional markets flash warning signs.

That desperation has fueled private credit's meteoric rise. But as TCW's leadership now warns, the foundation beneath this $2 trillion edifice may be built on sand.

The Party in the Soundproof Room

For fifteen years, while public markets obsessed over Federal Reserve announcements and quarterly earnings, a parallel financial system was quietly becoming the new backbone of corporate America. Private credit—direct lending by massive funds rather than regulated banks—exploded from a niche alternative to a dominant force.

The names are familiar: Apollo, Blackstone, Ares Management. These aren't fringe operators—they're Wall Street titans who saw an opportunity after the 2008 crisis. When Basel III and other banking regulations made traditional lending expensive and cumbersome, the demand for risky loans didn't vanish. The loans simply migrated from bank balance sheets to unregulated fund structures—a textbook case of regulatory arbitrage that would have made the architects of pre-crisis structured products proud.

What emerged was shadow banking in its purest form: all the economic substance of traditional lending, with none of the regulatory oversight. No capital requirements. No stress tests. No public disclosure of asset quality.

The Valuation Mirage

The most immediate vulnerability is also the hardest to quantify: nobody actually knows what these assets are worth.

When a bank makes a loan, mark-to-market discipline imposes a harsh reality. If the borrower deteriorates, the loan's value falls, and regulators force the bank to acknowledge the loss. Private credit operates differently. These loans don't trade, so funds value them using internal models—mark-to-model in industry parlance. The fund manager's spreadsheet becomes the arbiter of reality.

"The valuations are a fantasy," one former private credit manager told us on condition of anonymity. "You're being paid a fee based on the value you report. Do you think you're going to mark your assets down if you don't have to? You ride it until the wheels come off."

This opacity compounds as the assets move through the financial system. Insurance companies, desperate for yield in a prolonged low-rate environment, have become voracious buyers of private credit. They rely on "private letter ratings"—bespoke credit assessments that lack the scrutiny of public ratings. The Bank for International Settlements has warned explicitly about this practice, noting that it allows both funds and insurers to mask true risk exposure while maintaining the fiction of investment-grade portfolios.

The warning from TCW, which manages billions across multiple strategies, highlights precisely these concerns: the market's opacity, weaker protective structures compared to public debt, and the potential for cascading defaults once economic stress reveals the gap between modeled values and reality.

The Covenant Collapse

If opacity obscures the present danger, the erosion of loan protections has eliminated early warning systems for the future.

Traditional lending relied on maintenance covenants—contractual tripwires that gave lenders intervention rights before a borrower reached insolvency. Requirements to maintain minimum cash balances, debt-to-EBITDA ratios, or interest coverage metrics allowed lenders to restructure proactively or take control when companies deteriorated.

The modern private credit market has systematically dismantled these safeguards. Over 80% of deals now feature covenant-lite structures—loans with minimal or no financial maintenance requirements. Lenders have become passive passengers, unable to intervene until formal default occurs, by which point recovery prospects have typically evaporated.

This didn't happen accidentally. In a market where capital chased yield relentlessly, competitive dynamics drove a race to the bottom in credit terms. The fund willing to offer the weakest protections won the mandate. For a decade of easy money, it didn't matter—defaults stayed rare, refinancings were trivial, and everyone collected fees.

Now, as borrowing costs have surged and economic conditions tightened, those chickens are coming home to roost. Companies that would have breached maintenance covenants years ago—triggering renegotiations or restructurings—have instead been allowed to deteriorate to the point where recovery rates may prove catastrophically low.

The Liquidity Time Bomb

Perhaps the most dangerous structural flaw lies in how these funds are marketed and structured. Many private credit vehicles, particularly "evergreen" funds targeting smaller institutional investors and family offices, promise quarterly liquidity—investors can redeem every 90 days.

The assets backing these promises are anything but liquid. Private loans are locked up for five to ten years, with no secondary market for distressed sales.

Any banking historian recognizes this design flaw immediately. It's the same liquidity mismatch that has destroyed institutions from Northern Rock to Bear Stearns: short-term liabilities funding long-term illiquid assets. When redemptions spike—whether from performance concerns, external shocks, or simple correlation in investor behavior—funds face an impossible choice. They can impose gates, trapping investors and triggering panic, or they can conduct fire sales, destroying asset values and creating a self-fulfilling spiral.

The European Systemic Risk Board has explicitly warned about this vulnerability, noting that a spike in redemption requests could force "rapid sales of illiquid assets," amplifying market shocks precisely when financial systems are most fragile.

For a decade, the mechanism remained untested. Redemptions stayed manageable. Returns looked smooth, courtesy of mark-to-model valuations that never reflected true market stress. But as one veteran investor observed, "Everyone's a genius in a bull market. The question is what happens when someone finally wants their money back."

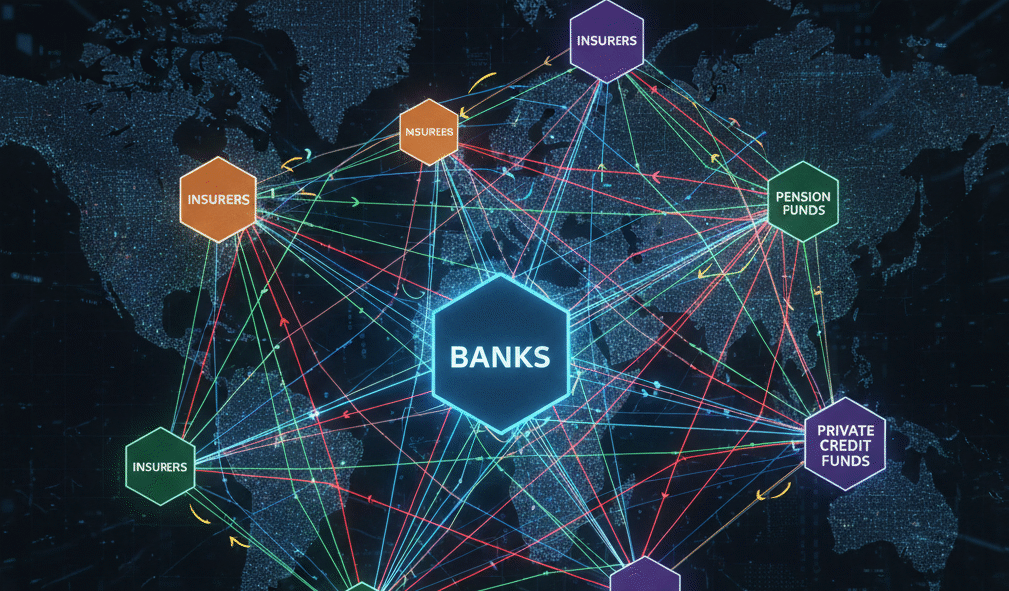

The Contagion Architecture

The systemic danger isn't confined to private credit funds and their direct investors. The architecture of modern finance has woven these structures into the fabric of the broader financial system in ways that create multiple pathways for contagion.

Major banks provide billions in "subscription lines"—revolving credit facilities secured by investor capital commitments. If funds face redemption pressure, they draw on these lines, directly exposing bank balance sheets to private credit stress.

Insurance companies have become the largest institutional investors in private credit, attracted by yield premiums that help them meet policyholder obligations. The BIS has documented how this exposure creates bidirectional risk: stress in private credit impairs insurance company solvency, while insurance company distress can force liquidations that crater private credit valuations.

Pension funds, desperate to meet return assumptions in a low-rate world, have steadily increased allocations. A crisis in private credit becomes a crisis in retirement security, with political implications that guarantee government intervention—though whether such intervention could be timely or effective in an opaque, contractually complex market remains doubtful.

When TCW warns it's "very nervous" about parts of private credit, the subtext is clear: the potential for cascading failures across interconnected institutions is real, and the industry's response mechanisms remain untested.

The Stress Test Arrives

For over a decade, benign conditions masked these vulnerabilities. Near-zero interest rates meant even weak companies could service debt. Refinancings rolled forward seamlessly. The fundamental fragility of covenant-lite, mark-to-model, liquidity-mismatched structures never faced genuine stress.

That era has conclusively ended. As markets demonstrated again on November 5, 2025—stocks falling for a second consecutive day, bonds rallying on safe-haven demand, the yen strengthening as global investors retreated from risk—the macro environment has fundamentally shifted.

Higher borrowing costs are squeezing the overleveraged middle-market companies that comprise private credit's core portfolio. Refinancing markets that once provided automatic extensions have turned hostile. The defaults that have been statistically absent are beginning to materialize, and recovery rates may prove shockingly low given the absence of covenant protections.

Equally concerning, the correlation in investor behavior is increasing. As traditional public markets become more volatile, institutional investors are reassessing risk across portfolios. The "denominator effect"—where falling public equity values automatically increase alternative investment allocations beyond policy limits—is forcing rebalancing. Redemption requests are rising.

The system is being stress-tested in real-time, and unlike regulated banks subject to Dodd-Frank's Comprehensive Capital Analysis and Review, there's no playbook, no regulatory backstop, and no transparent data to assess systemic exposure.

Regulatory Reckoning

Regulators have finally awakened to the danger, but they face the classic dilemma of shadow banking: the system has grown too large to ignore yet remains largely beyond their jurisdiction.

The International Monetary Fund's April 2024 Global Financial Stability Report dedicated an entire chapter to private credit, warning bluntly about data opacity, high leverage, and valuation practices that mask true risk. The Bank for International Settlements has flagged insurance company exposure as a particular systemic vulnerability. The European Systemic Risk Board has explicitly called out liquidity mismatches in retail-oriented structures.

The potential for increased regulatory scrutiny from the SEC and Federal Reserve is now inevitable. But the regulatory toolkit is limited. Unlike banks, private credit funds cannot be easily subjected to capital requirements or stress tests. They operate through private arrangements with sophisticated institutional investors theoretically capable of assessing risks themselves.

Yet as TCW's warnings demonstrate, even sophisticated market participants are struggling to assess true exposures. The opacity that makes private credit profitable also makes it nearly impossible to regulate effectively—at least until a crisis forces crude interventions like emergency lending facilities or ad hoc bailouts.

The historical pattern is consistent: shadow banking systems expand in regulatory gaps, grow until they're systemically significant, and then face regulation only after crises demonstrate their instability. We appear to be entering the final act of this familiar cycle.

The $2 Trillion Question

In late 2007, as concerns about subprime mortgages first surfaced, industry veterans and regulators offered reassurance. The exposure was contained. Markets were liquid. Sophisticated risk management had diffused systemic risk.

Within months, the global financial system was in free fall.

The parallel to private credit isn't perfect—no analogy ever is. But the structural vulnerabilities are strikingly similar: opacity that prevents accurate risk assessment, leverage that amplifies losses, covenant weakness that eliminates early intervention, liquidity mismatches that create run dynamics, and interconnectedness that creates contagion pathways.

Most concerning is the familiar complacency. For a decade of smooth returns and absent defaults, warnings about private credit were dismissed as academic hand-wringing. The system seemed stable precisely because it had never been tested.

Now the test has arrived. Interest rates have risen sharply. Economic growth is slowing. Market volatility has returned. Redemption pressures are building. And the $2.1 trillion private credit market—built on mark-to-model valuations, covenant-lite structures, and liquidity mismatches—faces its first genuine stress.

When TCW, an insider managing $433 billion with decades of market experience, says it's "very nervous," the message isn't subtle. The firm sees risks that others are still ignoring or minimizing. The opacity that has been profitable for so long is about to become dangerous.

The party is over. The only question is whether the exit will be orderly or whether, as in 2008, we'll discover that the emergency exits were never properly marked and the fire insurance was never actually purchased.

Markets have a habit of punishing complacency. The shadow banking system is about to be reminded of that lesson.

Sources & Further Reading

Bloomberg Law. (November 5, 2025). "Asset Manager TCW 'Very Nervous' About Parts of Private Credit." Direct industry warning from major institutional player regarding sector vulnerabilities.

International Monetary Fund. (April 2024). "Chapter 2: The Rise and Risks of Private Credit." Global Financial Stability Report. Comprehensive analysis of sector growth, opacity risks, and potential systemic implications.

Bank for International Settlements. (October 2025). "The transformation of the life insurance industry: systemic risks and policy challenges." Examination of insurance company exposure to private credit and contagion pathways.

European Systemic Risk Board. (September 2025). EU Non-bank Financial Intermediation Risk Monitor. Analysis of liquidity mismatch vulnerabilities in non-bank lending structures.

S&P Global. (2025). "Leveraged Commentary & Data (LCD)." Market data documenting prevalence of covenant-lite structures across leveraged lending markets.